Automating India: Investing in Robotics and the Future of Productivity

Just a few years ago, robotics felt like a distant frontier for Indian startups — technically ambitious, capital-intensive, and lacking the infrastructure or domestic demand to scale. That has changed. Robotics in India is fast becoming a practical, necessary, and scalable response to the structural demand for productivity across multiple sectors of the Indian economy.

India is scaling from $4T in GDP today to $10T and beyond over the next 15 years, presenting a generational opportunity to fundamentally rewire the physical systems that move goods, build and maintain infrastructure, and augment the supply chains of essential services.

Robotics at an Inflection Point: A Horizontal Layer Taking Shape

The global robotics market is approaching a structural inflection point. What was once limited to highly controlled specialist manufacturing environments is now expanding into dynamic, service-heavy sectors—from logistics and pharmaceuticals to agriculture and construction.

In 2023, the global install base of industrial robots crossed 4.28 million units, growing 10% year-on-year. Annual installations exceeded 540,000 units in 2024, marking the fourth consecutive year above the half-million mark. (World Robotics Report, IFR, 2025)

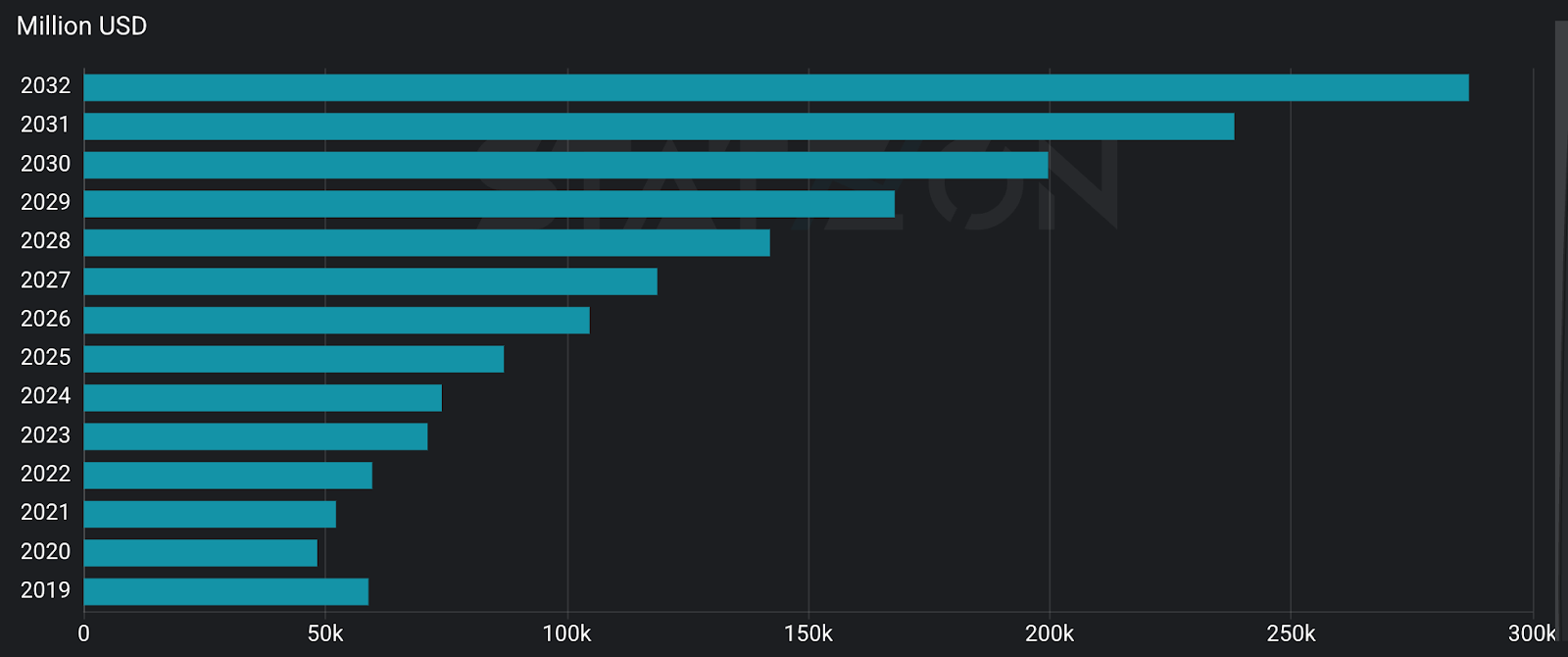

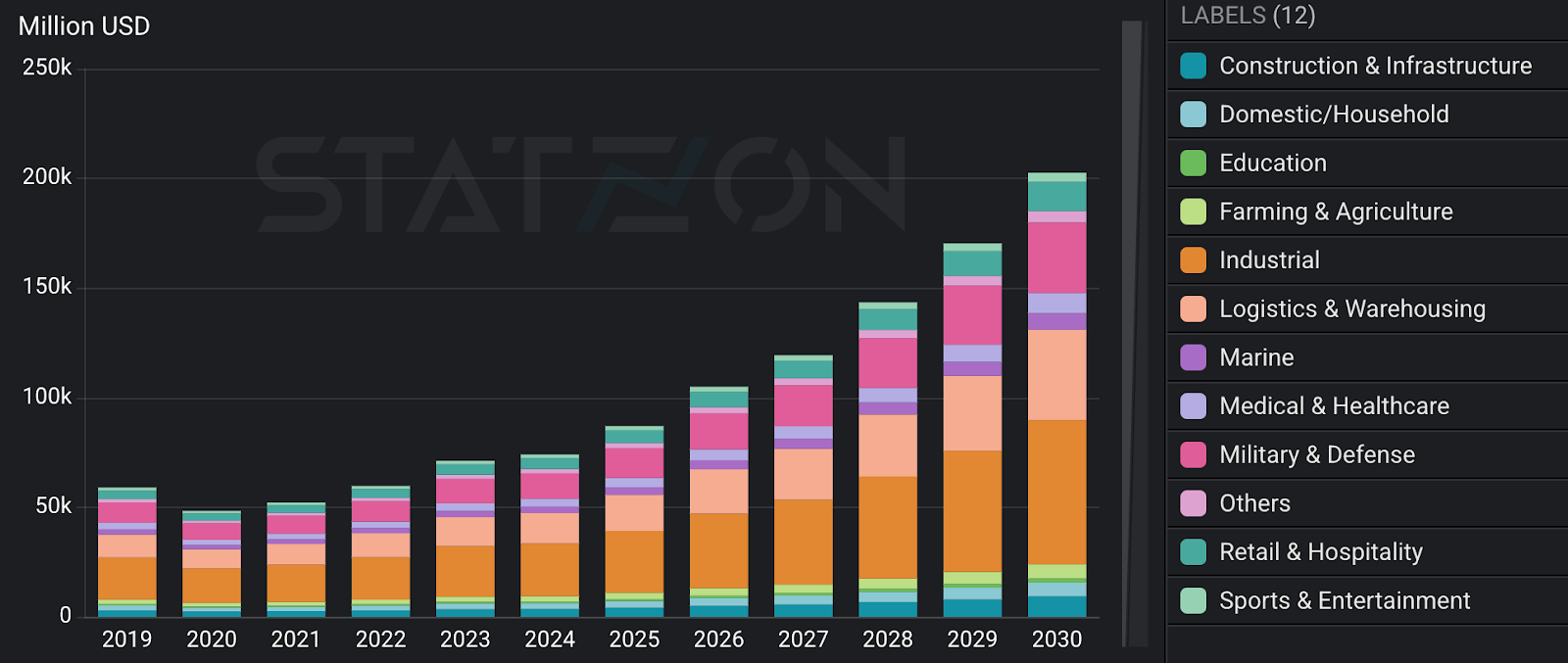

Global Robotics Market Value, by End-Users (US$ Mn)

Across all verticals, multiple macro shifts are making robotics more viable, even in traditionally under-automated industries:

- Declining hardware costs: Industrial robot unit costs have dropped nearly 25% over the last decade.

- Software-first orchestration: Centralised layers now manage task assignment, fleet coordination, diagnostics, and updates.

- RaaS models unlocking SME access: Monthly pricing bundles lower CapEx barriers for Tier 2 and 3 locations.

- AI-led performance uplift: Pre-trained models and simulation-based training reduce on-site learning cycles significantly.

Understanding the Stack: Categories, Capabilities, and Deployment Models

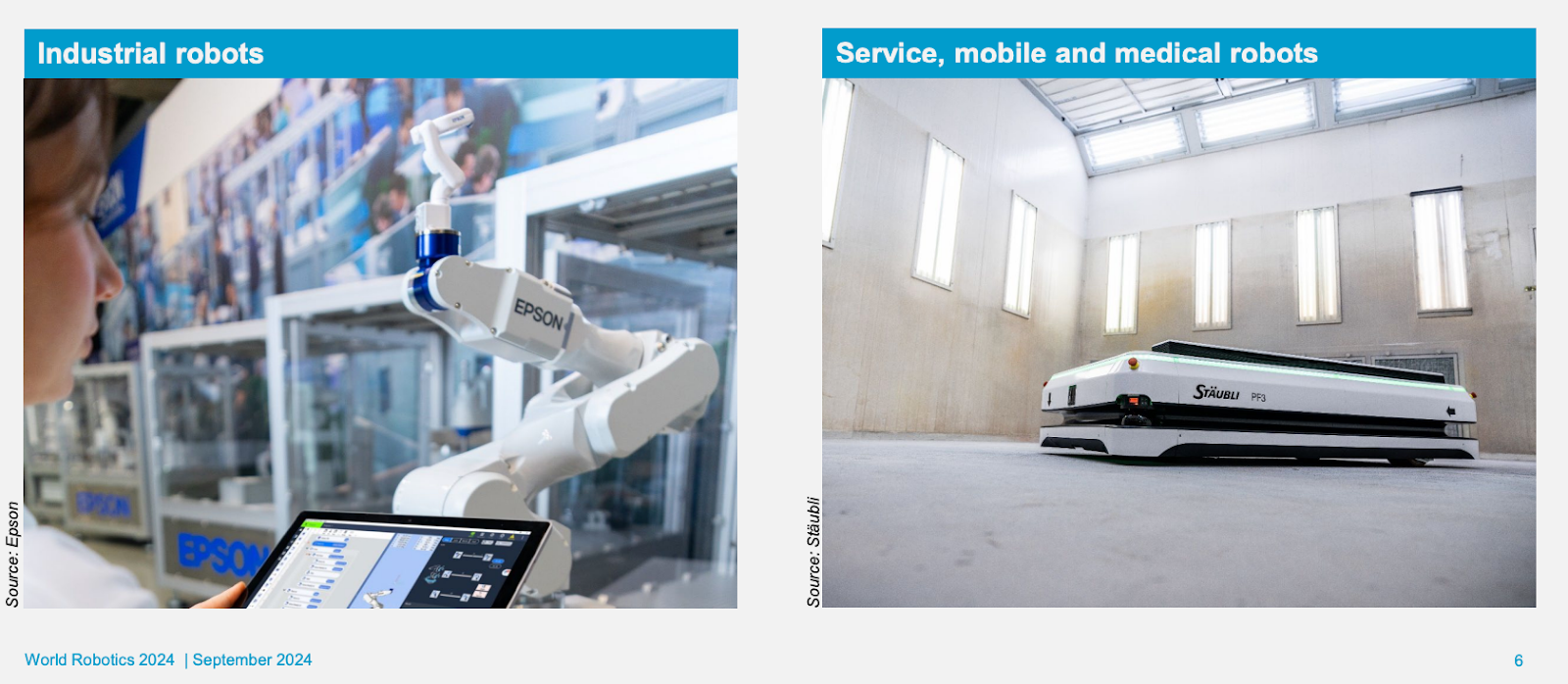

Robotics can be broadly segmented into industrial and professional service categories, differentiated by the nature of their environments, tasks, and control logic.

- Industrial robots are typically deployed in highly structured environments like factories, labs, and assembly plants. They are built for repeatability, speed, and precision.

- Service robots operate in less predictable environments—warehouses, hospitals, farms—and require higher degrees of sensing, navigation, and safety logic.

What gets adopted and scaled is a solution stack that solves a real operational bottleneck end to end. Three dominant playbooks have emerged:

- Application Playbook: Deep, vertically integrated solutions bundling hardware, software, and deployment tooling for pharma, defence, and agri processing.

- Product Playbook: Standardised, modular platforms like cobot arms, AMRs, and AGVs configurable across automotive, food, and electronics.

- Software Playbook: A hardware-agnostic SaaS layer covering robot control, task allocation, diagnostics, and performance optimisation.

Future winners will blend all three, owning the customer problem across the full stack.

Mapping the Global Landscape: Where Robotics Is Scaling, and Why

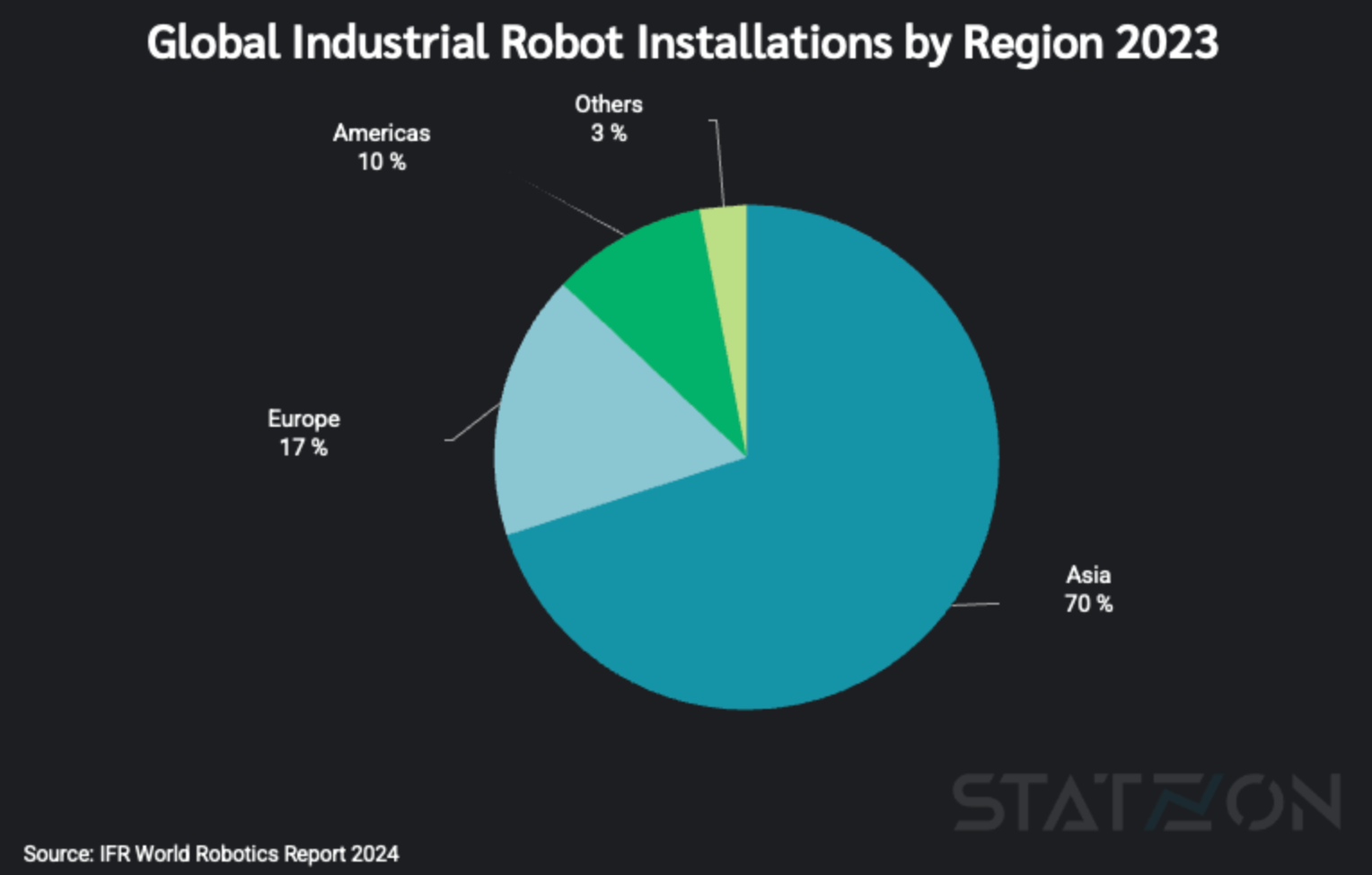

The current industrial robotics landscape is deeply regionalised. While the technology base is becoming global, the patterns of adoption remain shaped by national industrial priorities, cost structures, and demographic shifts.

In 2023, over 70% of all industrial robot installations were concentrated in Asia.

China alone accounted for more than half of global deployments. The remainder was split between advanced manufacturing hubs in Europe and logistics-led adoption in the United States. India, while still a small base, recorded the fastest growth globally.

Regional Breakdown: Installations and Use Case Priorities

Source: World Robotics Report 2025

Across regions, a few use cases consistently stand out: warehouse automation in the U.S., electronics and EV manufacturing in Asia, and cleanroom robotics in Japan and South Korea. Germany continues to push advanced cobots in automotive and machinery, while India is emerging in pharma, logistics, and EV assembly. Globally, the strongest signals are coming from logistics, precision manufacturing, and healthcare-linked applications. That’s where the next decade of automation is compounding fastest.

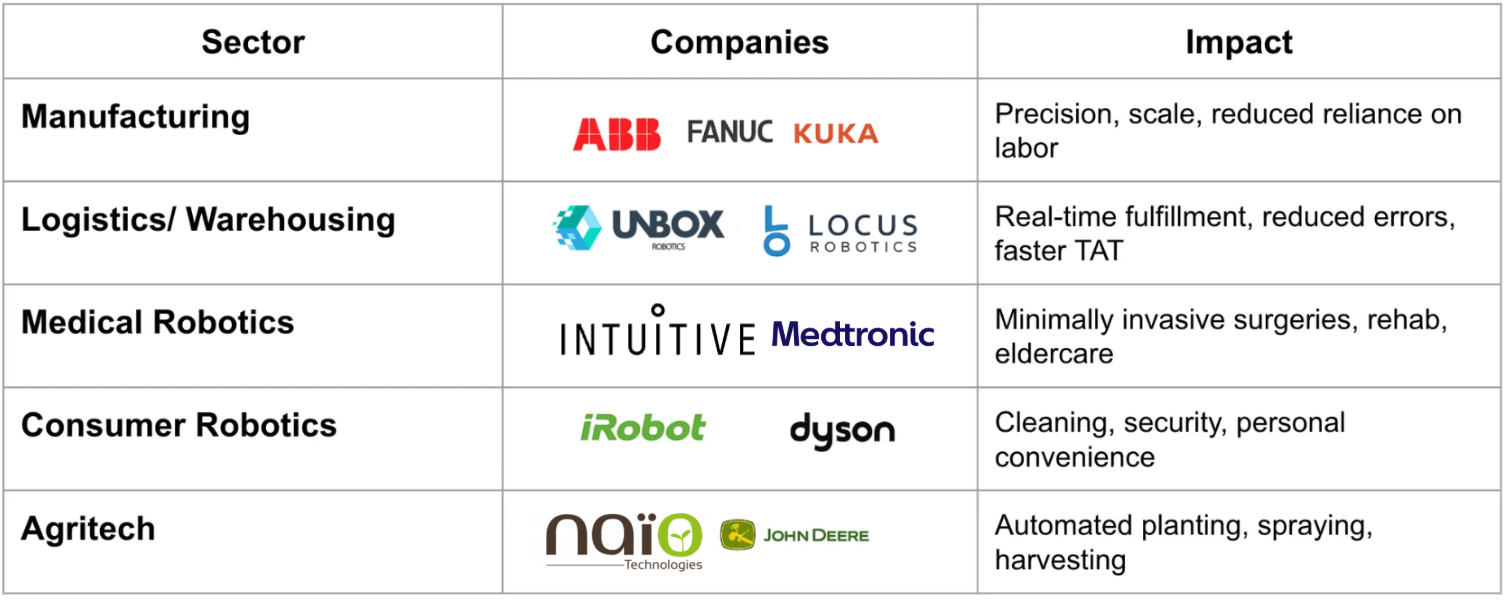

Across sectors, global robotics leaders succeeded by targeting large markets with critical productivity gaps and margin pressures—solving real pain points rather than pushing novelty. Whether in manufacturing (ABB, Fanuc), logistics (Ocado, Locus), or healthcare (Intuitive Surgical), they didn’t aim to replace humans, but to augment capability and reduce operational friction.

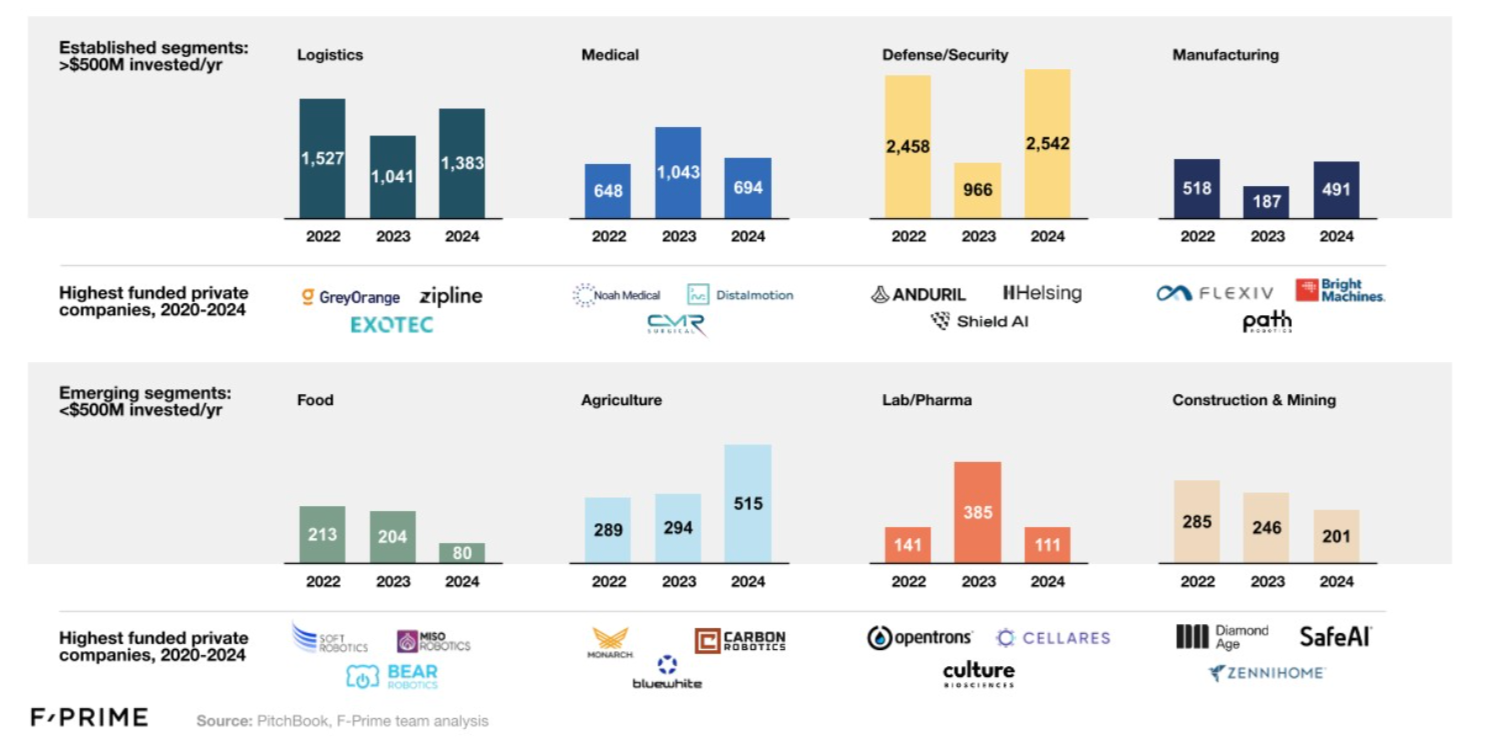

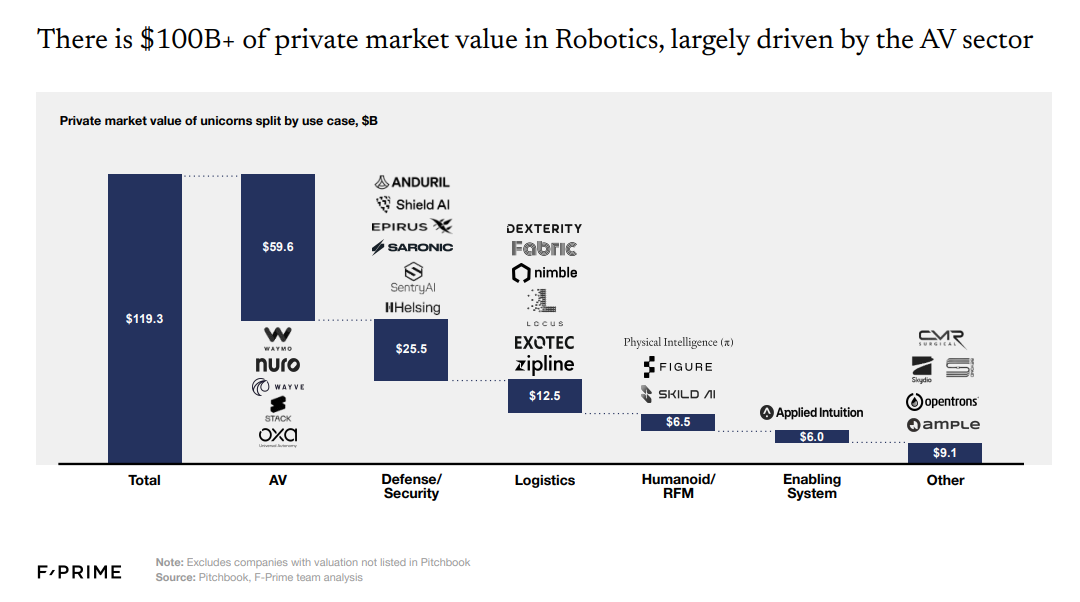

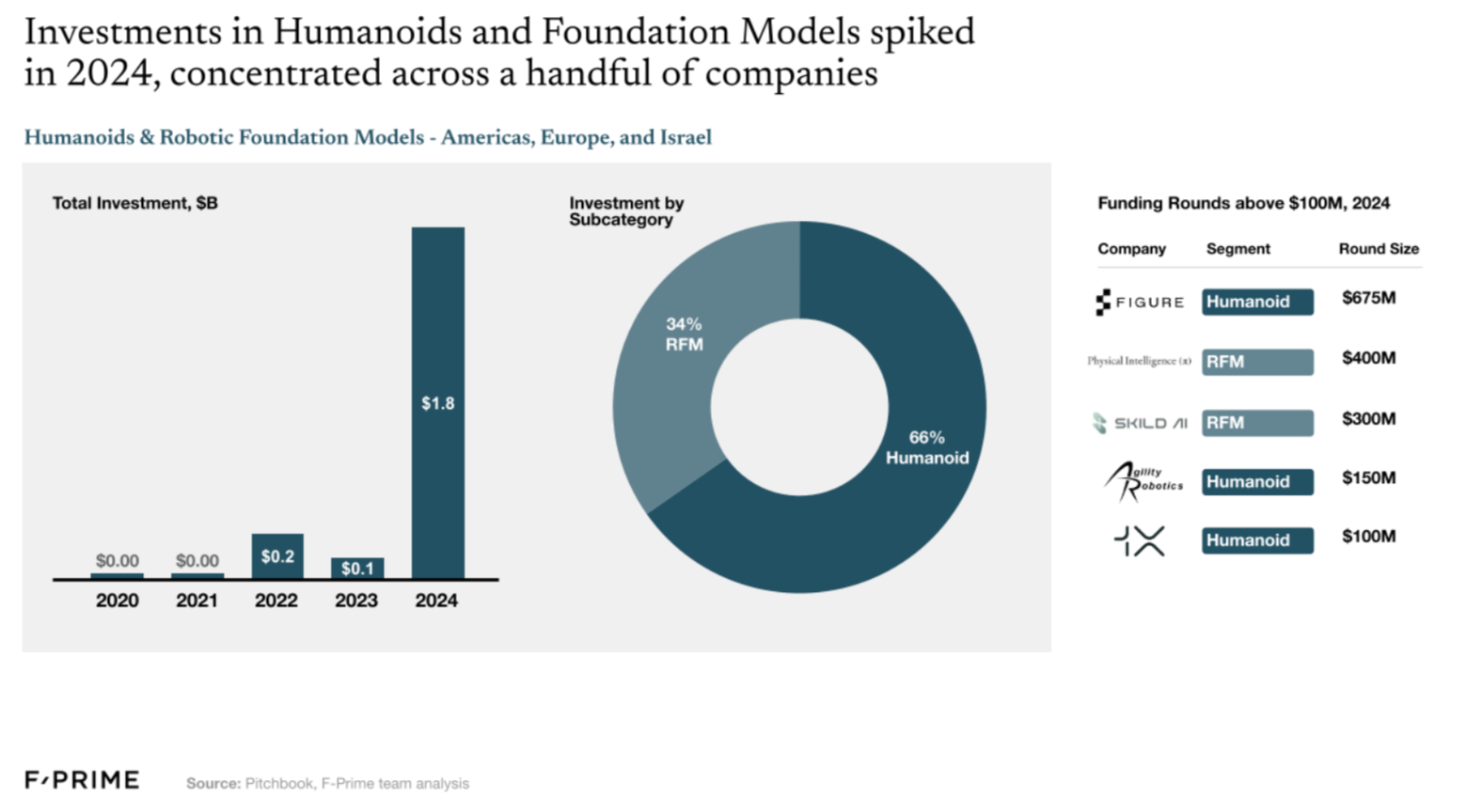

Investment trends in evolved markets like the America and Europe are witnessing a surge in investments across more technically superior uses cases. In 2024, robotics investment across the US, Europe, and Israel hit $18.6B, more than doubling from the previous year (F Prime analysis)The biggest capital flows went to autonomous vehicles ($8.4B), as investors doubled down on real-world deployment of driverless and delivery fleets. Vertical robotics—targeting sectors like logistics, healthcare, defense, and manufacturing—attracted $7.1B, reflecting clear ROI in industry-specific use cases. Meanwhile, humanoids and foundation model-led bots saw $1.8B in funding, and enabling systems like LiDAR, sensors, and component stacks raised $1.3B. The momentum in these regions shows capital is following mature deployment rails and full-stack automation themes.

India’s Strategic Opportunity

India reached a record 9,120 robot installations in 2024, a 7% increase year-on-year, making it the sixth-largest installer worldwide. Automotive led with installations surging 15% to 4,070 units, plastics and chemicals grew 33% to 600 units, and the metal industry grew 30% to 420 units. With GDP growth projected at 6.5% in 2024-2025 and continued EV investments, India's robotics market is set to expand further.

(Source: IFR World robotics report 2025 India PR)

India’s robotics startups funding jumped from $28.8M (2022) → $54M (2023) → $117M (2024) across 40+ deals (Economic Times) Global robotics startups raised $18.6 billion in 2024, more than double the $8.6 billion recorded in 2023. India's advantage is 10x cheaper prototyping and 2x faster deployments than the West.

Source: Tracxn

India's manufacturing sector is embracing Industry 4.0, with Flipkart deploying 100 warehouse robots processing 4,500 packages per hour. Robot density remains low at 7 per 10,000 workers against a global average of 141, constrained by CapEx sensitivity, working capital costs, integrator fragmentation, and reliance on imported subsystems.

Where Founders Can Build: Our India Opportunity Map

1. Warehouse Automation

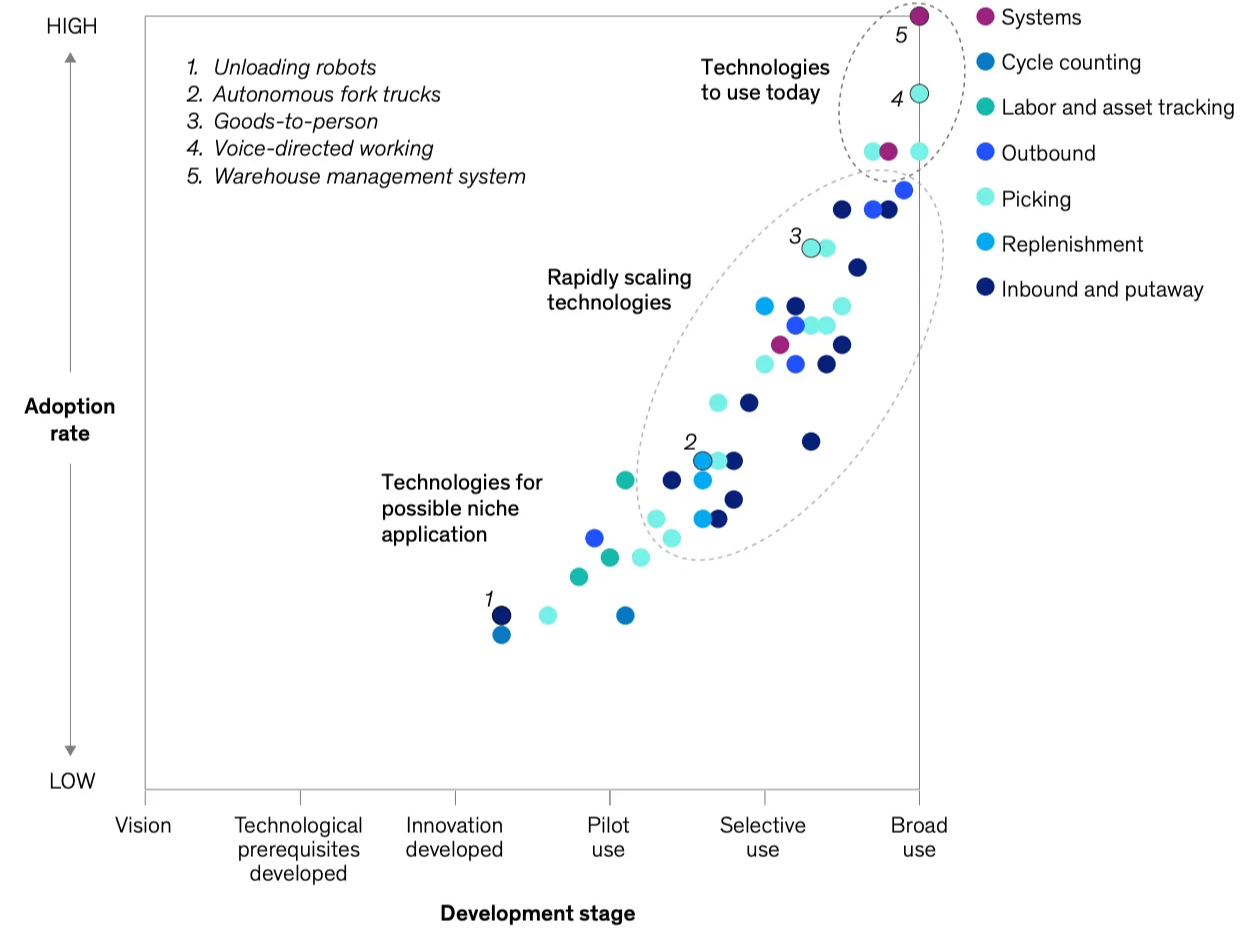

India's warehousing ecosystem is under pressure from e-commerce, D2C brands, and global trade, all pushing toward high-speed, low-latency fulfillment, with labor volatility and rising costs making 24/7 automation a functional requirement. The Indian warehouse automation market was valued at $712.9 million in 2024, and is projected to grow to $2.6 billion by 2033, at a CAGR of 15%, accelerated by the Make in India policy push, rapid digitisation, and rising input costs across the logistics value chain. Unbox Robotics, Addverb Technologies, and Armstrong are already deploying end-to-end systems including AMRs, robotic sorters, smart conveyor units, and WMS-integrated platforms, with Flipkart deploying 100 sorting robots at a Bengaluru hub processing over 4,500 packages per hour.

Source: McKinsey - industrial robotics; Warehouse automation technologies, by development stage and adoption rate:

What can be built:

- ASRS systems optimised for India’s vertical constraints

- AI-powered picking and sortation bots that adapt to mixed inventory

- Cloud-based orchestration layers that integrate seamlessly with WMS and IoT sensor networks

Robotics is expanding into retail environments through restocking bots, robotic kiosks, and autonomous carts, linking last-mile logistics directly with in-store operations. Full-stack solutions combining hardware, orchestration, and deployment via RaaS models represent the next frontier.

2. Industrial Assembly & SME Manufacturing

India's vast industrial base is under-automated across SMEs in auto components, electronics, and precision fabrication, with the real whitespace in making cobots and vision-enabled tools viable for Tier 2 and Tier 3 units.

What’s being built:

- Systemantics, CynLr are solving for vision and perception in dynamic shop floors

- Peer Robotics are focused on cobots for component handling and assembly

- Universal Robots (India) is scaling SME adoption in automotive and FMCG

Large enterprises have begun automating material handling and sorting, but these workflows are only beginning to reach India's SME manufacturing base.

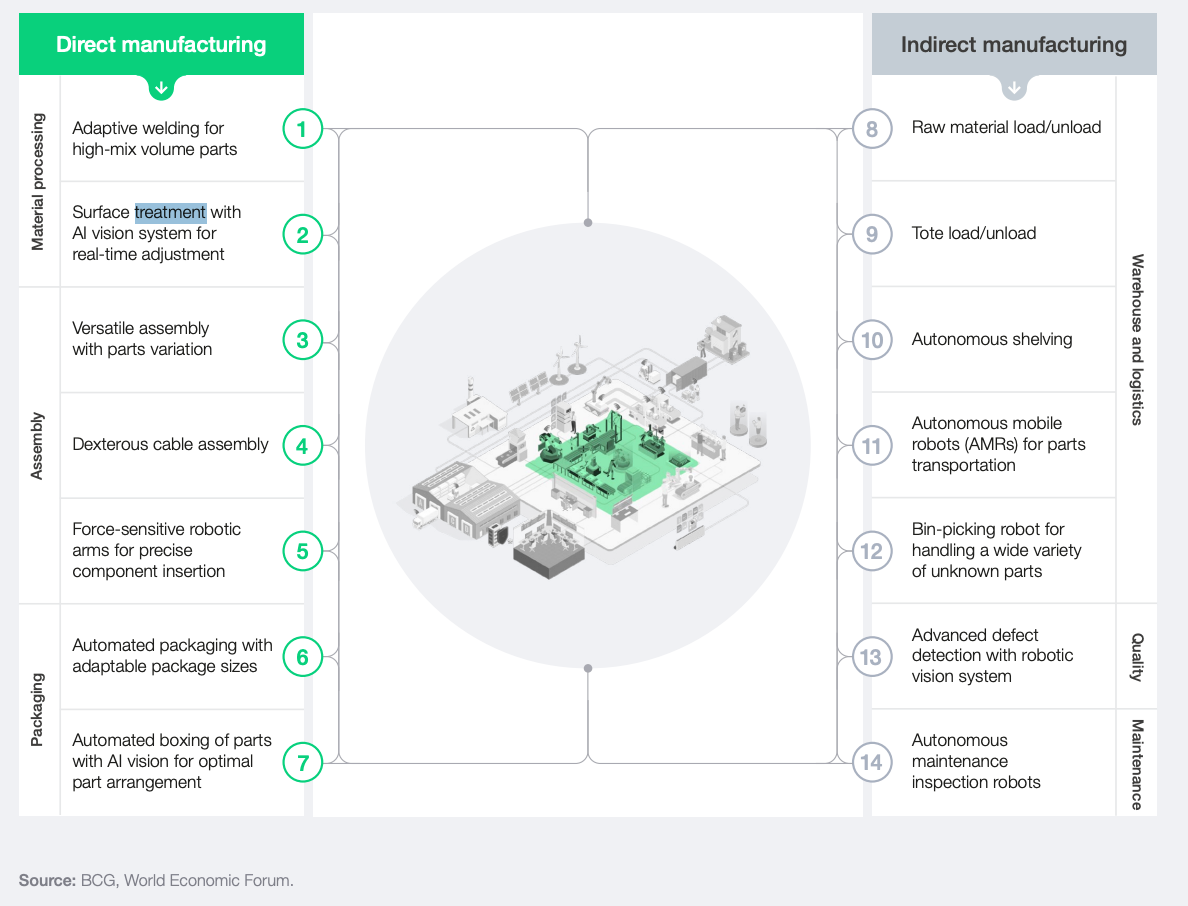

How physical AI is reshaping factory and warehouse operations Source: BCG/ WEF report

Precision assembly and welding remain largely manual across Indian MSMEs, creating a clear opportunity for affordable, programmable robotic arms that augment skilled workers.

What can be built:

- Modular, programmable arms with minimal setup time

- AI-led inspection tools for pharma, electronics, auto

- Robotic kits tailored for retrofit into constrained MSME floors

AI-enabled robotic quality assurance for real-time defect detection across auto, electronics, and consumer goods represents an additional opportunity, built as vision-based QA arms, compact systems for small-batch manufacturers, and cloud-connected systems that learn from edge error data.

3. Medical & Assistive Robotics

India’s healthcare system is capacity-constrained—both in clinical talent and infrastructure reach. Robotics can offer augmentation where gaps are structural: surgical precision, hospital hygiene, patient logistics, and post-operative rehab.The Indian medical robotics sector was sized at 1.32 billion in 2024, and is projected to reach USD 8.1 billion by 2033, growing at a CAGR of 21%. The fastest-growing segments are surgical robotics, hospital service bots, and rehabilitation systems, with focus shifting from R&D prototypes to commercial deployment priced well below global counterparts.

What is being built:

- SS Innovations has built the SSI Mantra, a surgical system designed for affordability and reliability in Indian hospitals

- Dozee has built FDA-cleared AI-driven remote patient monitoring systems that predict vitals deterioration in real time

- Aether Biomedical and Makers Hive are developing bionic limbs with embedded sensors and cloud connectivity

- Astrek Innovations is building wearable exosuits for mobility recovery

- Invento Robotics has deployed patient service and disinfection bots in hospitals

What can be built:

- Affordable surgical systems for Tier 2 and Tier 3 hospitals at one-third global costs

- Rehab and assistive devices for post-op and eldercare via RaaS and subscription pricing

- Hospital service bots for sample movement, disinfection, and patient interaction across mid-sized hospitals

An adjacent opportunity lies in life sciences automation for diagnostics, CROs, and labs, where modular robotics for pipetting, liquid handling, and sample prep integrated with AI-led QC and lab informatics can underpin India's diagnostics and research scale-up.

4. Autonomous Surveying Robots

Surveying is fundamental to infrastructure, agriculture, mining, and public utilities, but traditional methods are slow, risky, and manpower-intensive. Autonomous aerial and underwater robots offer a faster, safer, and more scalable way to collect data, especially in hard-to-reach or hazardous zones. Globally, the surveying robot market is growing at a 12.3% CAGR, from $1.2 billion in 2024 to a projected $3.5 billion by 2033.

What’s being built:

- ideaForge, Aereo, Asteria Aerospace, are deploying drones for defense, asset inspection, mining, and infra audits

- Underwater surveying is nascent but growing, driven by academic spinouts targeting dams, pipelines, and ports. Planys is a pioneer in this category.

What can be built:

- Aerial drones for land, agriculture, and infrastructure surveys

- Underwater robots for asset inspection in dams, pipelines, and ports

- AI-powered analytics and mapping platforms integrated with public utility and EPC systems

India's rugged geography and infrastructure spend create strong domestic demand, with significant export potential across Africa, Southeast Asia, and Latin America.

5. Agricultural Robotics

India’s agriculture sector is large, but highly fragmented. Over 80% of farms are under two hectares, with wide variability in soil, irrigation, and crop cycles. The domestic market is constrained by adoption friction, CapEx sensitivity, and service complexity, making India a difficult market for at-scale monetisation but an ideal testbed for globally scalable solutions.

What is being built:

- TartanSense builds compact field robots for precision weeding and spraying

- Fasal and Farms2Fork deploy drone and satellite data-based monitoring tools

What can be built:

- Rugged seeding, spraying, and weeding robots for small, diverse plots

- Ground and aerial systems for horticulture and high-value crops

- Autonomous tractors, harvesters, and soil diagnostics platforms via leasing or agri-input partnerships

The path to scale runs through agri-cooperatives, FPOs, and cross-border deployment into Africa, Southeast Asia, and Latin America.

6. Construction Robots

India’s $5.6B construction robotics market is being shaped by labor shortages, tighter safety mandates, and the sheer pace of infrastructure rollout. As the country builds out smart cities, highways, metros, and mass housing—all in parallel—the demand for speed, quality, and consistency on-site has never been higher. The Global Construction Robots Market size was estimated at USD 1.4 billion in 2024 and is projected to reach USD 3.66 billion by 2030, growing at a CAGR of 18% from 2025 to 2030

Early adopters are concentrated in public infrastructure and EPC players, with forward-leaning private developers beginning to explore robotics in premium high-rise and commercial real estate.

What is being built:

- Flo Mobility specialises in autonomous technology for material movement and micromobility

- L&T and Tata Projects are running site pilots for robotics in repetitive and hazardous tasks

What can be built:

- Task-specific robots for bricklaying, painting, and facade maintenance

- Mobile 3D printing units for low-cost housing and modular infrastructure

- Inspection and safety bots for confined space or vertical sites

The investable plays will be wedge-first solutions targeting one repeatable job, deployment-ready systems that plug into existing workflows, and financially structured via RaaS or leasing aligned with developer cash cycles.

7. Urban Infrastructure & Cleaning Robotics

Municipalities face growing pressure to automate dangerous and costly manual infrastructure processes.

Globally, the urban cleaning robotics market is estimated at $6 billion (2024) and projected to grow to $21 billion by 2030. While India-specific data isn’t broken out separately, this segment is a fast-growing layer within the broader Indian robotics market, which is expected to grow from $1.7 billion (2024) to $6.81 billion (2033) at a 16.4% CAGR.

What’s being built

- Genrobotics: Sewer-cleaning robots (Bandicoot), deployed across Indian cities

- Peppermint: Commercial floor cleaning robots for malls, airports, and offices

- Municipal drone pilots for city asset mapping and infrastructure audits

What can be built

- Robotic road sweepers for highways, metros, and smart cities

- Autonomous sewer inspection and cleaning bots for municipal networks

- Drones for pollution monitoring, utility inspection, and 3D asset mapping

8. Consumer Robotics (Niche, but Growing)

Rising incomes and smaller households are driving demand for domestic automation.

Globally, the consumer robotics market is projected to grow from $11 billion (2024) to $40 billion by 2030. In India, the segment is nascent but growing, with service robotics (including consumer) expected to reach $430 million in revenues by 2025.

What’s being built

- Milagrow Entry-level domestic cleaning bots

- Academic labs working on eldercare and social humanoid prototypes

What can be built

- Floor cleaning and vacuum bots for apartments and villas

- Home surveillance robots and mobile camera patrol units

- Companion and eldercare robots for assisted living and mental wellness

India's opportunity lies in building frugal, reliable robots for emerging markets.

9. Robotics for Space Applications

India's space sector is scaling through ISRO missions and an emerging private ecosystem.

Globally, the space robotics market is expected to grow from $5 billion (2024) to $8.5 billion by 2030. India is still early, but investment is rising via Chandrayaan, Gaganyaan, and commercial satellite programs.

What is being built:

- ISRO is developing robotic arms for modular space stations and rovers for lunar operations

- Private startups and university spinouts are exploring zero-gravity robotics, docking tech, and micro-satellite servicing

What can be built:

- Robotic crawlers and arms for spacecraft maintenance

- Science experiment platforms for low-gravity environments

- Planetary exploration robots for cost-constrained missions

Startups that solve for extreme payload limits, power optimisation, and remote operability can plug into global aerospace supply chains as an export-first play.

10. Mapping Emerging Frontiers in Indian Robotics

A few categories signal where India's robotics narrative expands over the next decade, with activity picking up across four emerging frontiers.

- Defense Robotics: UGVs, surveillance drones, and unmanned logistics platforms are being piloted across DRDO programs, with the real opportunity in dual-use robotics for emerging markets where India can price and ruggedise competitively.

- Smart Logistics and IIoT: AMRs are integrating with fuel sensors, thermal monitoring, and predictive maintenance stacks, with the biggest opportunity in hardware-software bundles across perishables and pharma.

- Autonomous Mobility: Controlled ecosystems like campuses and industrial parks are already piloting AV use, with Swaayatt building autonomy kits for bounded networks and an export play in autonomy-as-a-service for gated environments.

- Humanoid Robotics: Invento is shipping humanoids into banks and hospitals, with the edge lying in packaging known components into affordable, low-maintenance service bots for emerging markets.

2024 saw a breakout year for humanoids and robotic FMs in the US–EU–Israel corridor, with $1.8B raised—two-thirds flowing into humanoid platforms.

Policy Tailwinds That Make This a Decade-Long Opportunity

India's policy framework is aligning with its robotics ambitions across four key instruments.

- The PLI scheme has expanded to 14 sectors with increased allocations for electronics, IT hardware, and auto components, bringing precision systems, mechatronics, and factory automation into direct scope.

- The Semicon India initiative, backed by a $10 billion allocation, targets chip import dependency, directly impacting availability of motion controllers, sensors, and vision chips.

- The Draft National Robotics Strategy outlines priority use cases in manufacturing, agriculture, healthcare, and defence, with a two-tier governance model to accelerate R&D and commercialisation. (Draft national strategy)

- SAMARTH Udyog Bharat 4.0 targets MSME supply chain digitisation, complemented by skilling programs including NAMTECH and ABB Robotics School.

Thesis in Action: Unbox Robotics

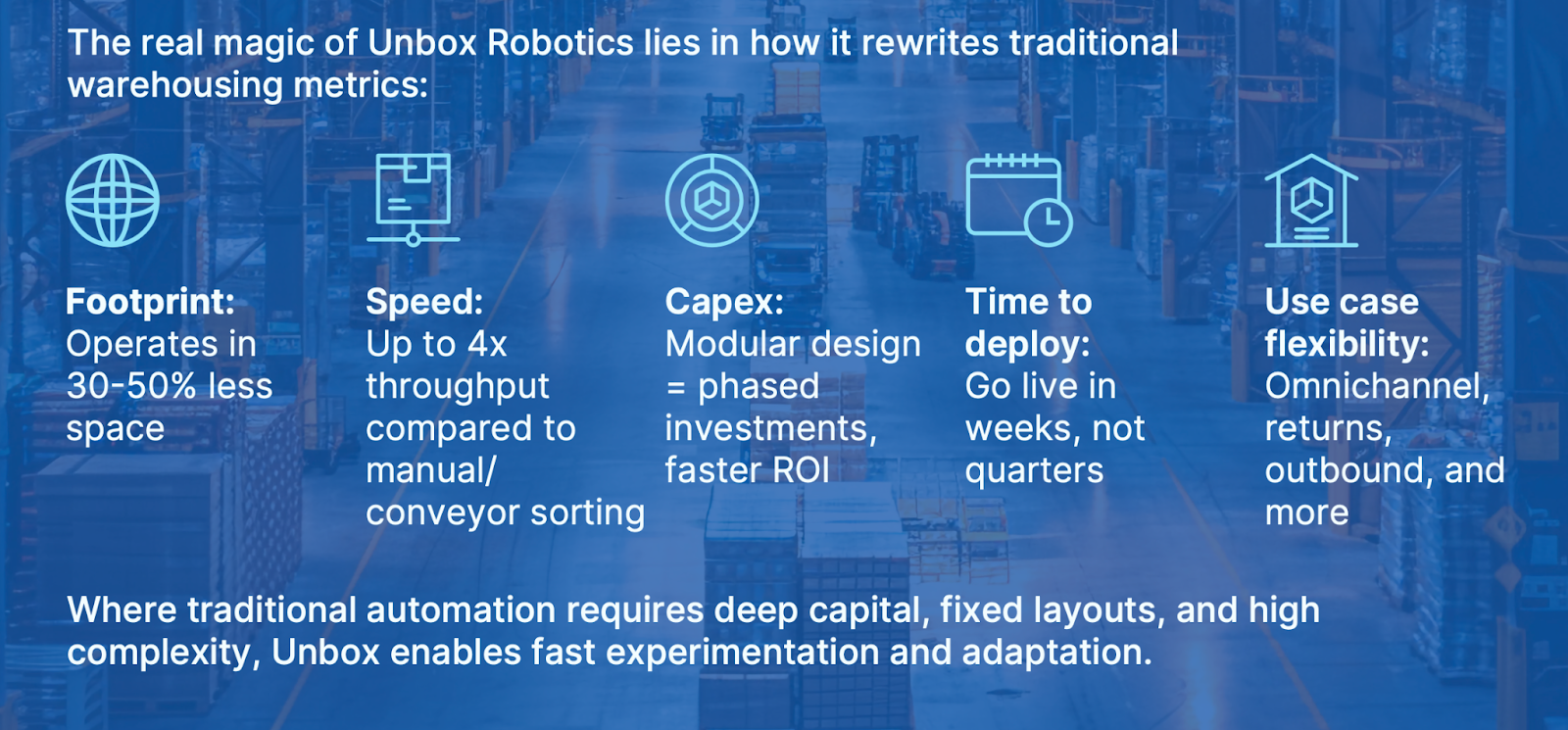

3one4 Capital backed Unbox Robotics to solve a deeply Indian problem: sorting millions of parcels per day inside constrained warehouse footprints in Tier 1 and 2 cities where real estate is expensive and labor is volatile.

Their flagship platform, VertiPick, uses vertical swarm robotics to sort parcels upward, cutting required warehouse space by 50% and boosting throughput by 2 to 4 times versus conventional systems. From that base, they have evolved into a full-stack warehouse automation platform spanning:

- PalletMove: Autonomous forklift-grade robots for intralogistics

- CubbyTrain: Mobile cubby units for bulk sortation in 3PL hubs

- VersatilePick: Mobile manipulators for trailer loading and palletising

- General Purpose AMRs: Adaptable platforms for bin movement and dynamic workflows

Unbox is now live across 10 or more enterprise-grade sites in India, the UK, the US, Spain, the Netherlands, and Italy, covering omnichannel sortation for fashion retailers and returns processing for global 3PLs. Unbox sells outcome-layer automation as a fully integrated product, software, and orchestration stack delivered via RaaS.

How India Can Build a Global Robotics Champion

Demand is visible, policy tailwinds are in place, and the next phase requires founders who can solve for deployment, GTM, and business model fit alongside product.

- Design for Constraints. Sell to Scale. Engineer for dense, unpredictable environments on modular, localised supply chains that drive down cost-per-task.

- Anchor in Use Cases Where Delta = $$ The highest-conviction opportunities are intralogistics, SME manufacturing, and medical robotics where talent gaps create high willingness to pay.

- Adopt Business Models That Fit Indian Realities RaaS for warehousing and pharma; leasing for SME floors; pay-per-use for drones and inspection bots.

- Hire Like a Systems Company, Not a Mech Lab Blend controls, mechatronics, vision, and AI with deep deployment operations.

- Treat India as Proof. Not the Ceiling. What works here scales to SEA, MEA, the Global South, and brownfield markets in the EU and US.

What Will the Outliers Look Like?

They’ll look less like robotics startups, more like automation infrastructure companies:

- Tight hardware-software orchestration

- Deployment playbooks across 5+ verticals

- Business models aligned to buyer economics

- Global delivery capabilities

- Deep working capital and lease finance relationships

They won’t be building a robot, they’ll be building India’s automation rails. And they’ll be built to last.

India's startup DNA is primed for this challenge, with founders who have built full-stack, asset-light platforms combining technical resilience with breakthrough design, and an IT services track record that has demonstrated the ability to win global markets.

For founders, this is a multi-decade canvas with whitespace across sectors and geographies. For investors and policymakers, this is a foundational shift in how India produces, moves, and delivers value. The question is who will build it, and how fast.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)

-p-500.webp)

.jpg)