.jpg)

India’s Industrial Policy is Evolving into an Operating System. The Conditions for Founders to Build National Champions are Emerging.

Indian industrial policy is no longer behaving like a routine list of departmental schemes. It is being assembled into an operating system.

Since 2021, the Indian State has set two structural shifts in motion at the same time, and they are compounding.

1. Global re-integration through a dense lattice of Free Trade Agreements.

2. Sovereign self-reliance through a stack of National Technology Missions backed by hard budgetary outlays.

Read separately, each looks like familiar policy. Read together, they describe a State sequencing demand, capital, policy, and supply chains with intentionality India has not shown in a generation. The investment implications are tangible, and they are already visible in the order books of Indian exporters, the project pipelines of frontier technology missions, and the traction curves of companies in our own portfolio.

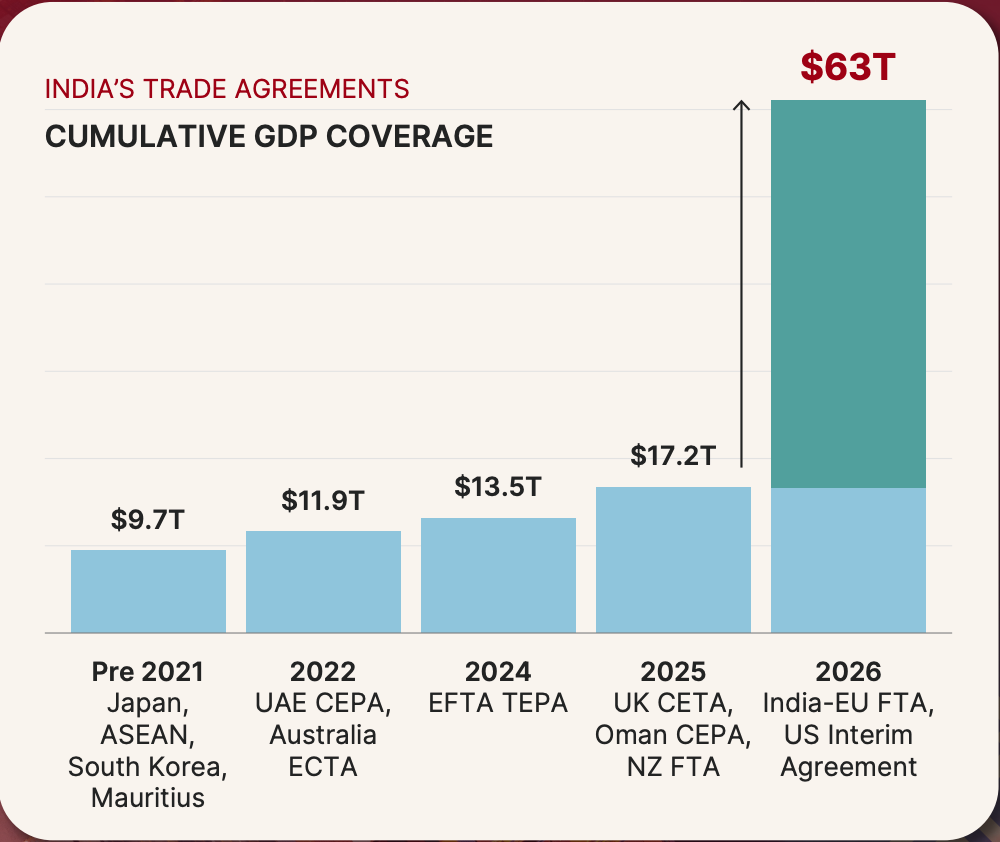

The Trade Architecture Has Been Rebuilt in Five Years

India entered this decade with preferential trade access to less than 10% of global GDP. By May 2026, that footprint has expanded to roughly 57%. The economies India can now sell into on preferential terms represent over $63 trillion in combined GDP and $615 billion in annual bilateral trade. This is the most ambitious trade reintegration India has undertaken since the WTO accession era.

Before 2021, India’s preferential trade architecture rested on four agreements with Japan, ASEAN, South Korea and Mauritius, covering roughly $9.7 trillion of partner GDP. Each was useful in its time, but built for an earlier global trade equilibrium.

The pace then sharpened. The UAE CEPA, signed in 2022, has already taken bilateral trade past $100 billion, with a new target of $200 billion by 2032. The Australia ECTA, also from 2022, has begun the transition toward a fuller Comprehensive Economic Cooperation Agreement. The India-EFTA Trade and Economic Partnership Agreement, signed in 2024 and entered into force on 1 October 2025, locked in a binding $100 billion investment commitment from Switzerland, Iceland, Norway and Liechtenstein over fifteen years. It is the first FTA in Indian history with a hard investment floor written into the treaty text.

Through the second half of 2025, the cadence accelerated further. The India-UK Comprehensive Economic and Trade Agreement was signed on 24 July 2025, delivering duty-free access on 99% of Indian exports to Britain with a stated target of doubling the $56 billion bilateral trade relationship by 2030. The India-Oman CEPA, signed on 18 December 2025, opens 98% of Omani tariff lines duty-free to Indian goods. The India-New Zealand FTA, concluded on 22 December 2025, offers immediate zero-duty access on 100% of New Zealand tariff lines.

The two largest deals followed in early 2026. The India-EU Free Trade Agreement was concluded at Hyderabad House on 27 January 2026, covering an economic bloc that represents roughly 25% of global GDP and a consumer market of approximately two billion people. Legal vetting is in progress. The European Commission expects entry into force in early 2027.

The United States and India announced an Interim Trade Agreement framework on 6 February 2026 that cut reciprocal US tariffs on Indian goods from 25% to 18% and then 10%, and committed India to $500 billion of counter-purchases over five years across American energy, technology, aircraft and critical materials. Finalisation is underway as both sides renew the urgency towards closure.

For Indian exporters in specialty chemicals, electronics, engineering goods, marine products, textiles, electrical equipment, and gems, the unit economics of expansion have moved. Phased duty elimination across the EU, UK, EFTA, Gulf, and Oceania means production decisions that previously failed the hurdle rate now clear it. This is the demand condition for an entire generation of Indian companies being levelled up.

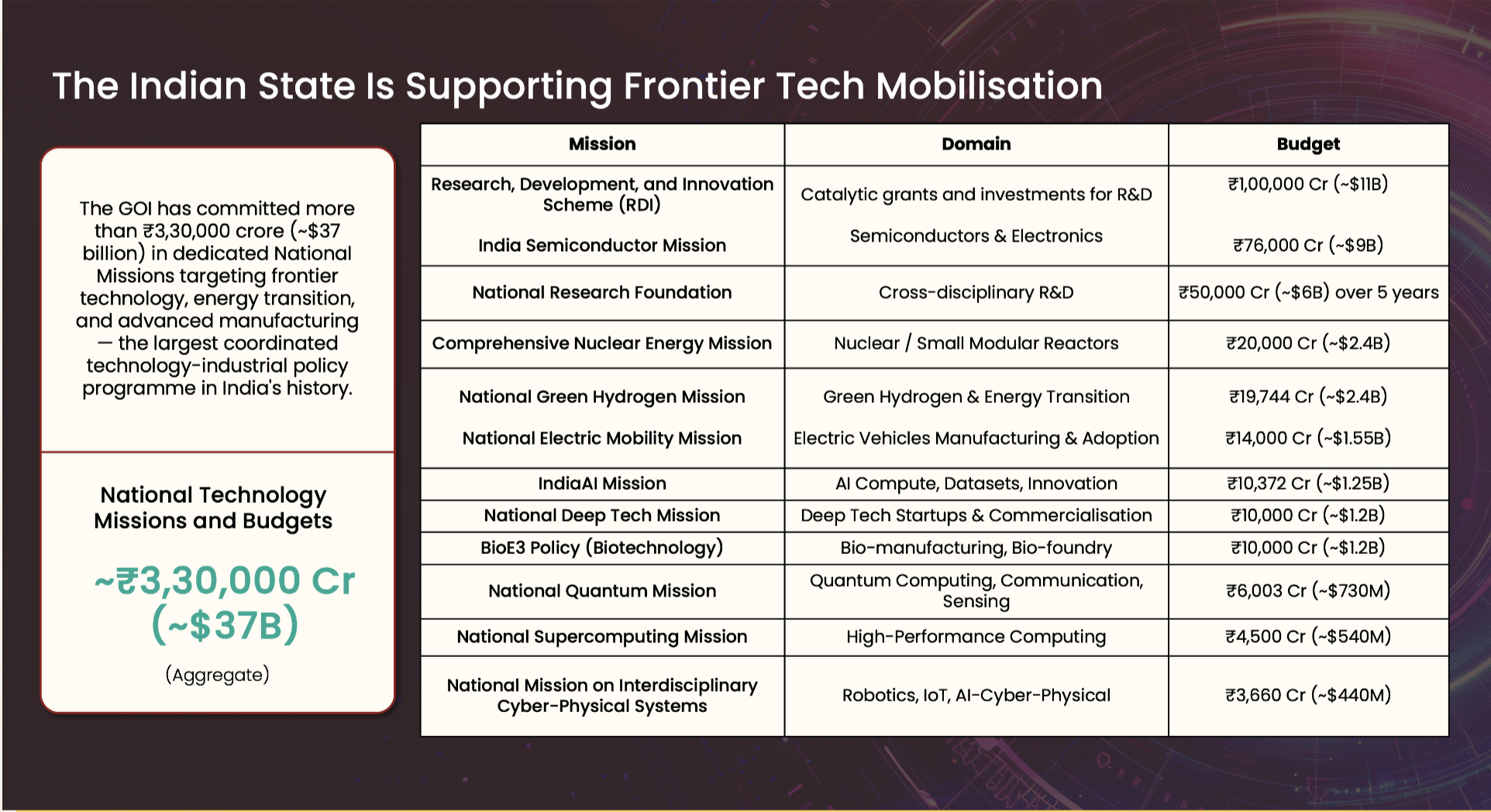

The State Has Built a Mission Architecture Around Sovereign Priorities

The trade architecture is one arm. The other is a coordinated stack of over a dozen National Technology Missions with combined committed outlays exceeding ₹3.3 lakh crore. The deployment cadence over the last twelve months has separated this generation of missions from the announcement-only patterns of earlier industrial policy.

The architecture has three tiers.

• The first is horizontal R&D capacity building. The Research, Development and Innovation Scheme (RDI), with a ₹1 lakh crore corpus, was approved by the Union Cabinet on 1 July 2025 and formally launched by the Prime Minister on 3 November 2025. It channels long-tenor and near-zero-interest capital through Alternative Investment Funds and Development Finance Institutions into private business R&D in sunrise sectors. The Anusandhan National Research Foundation (ANRF) carries a ₹50,000 crore corpus over five years for academic and translational research, with industry and philanthropic capital blended in. Together they form the largest pool of patient grant capital India has ever assembled for indigenous innovation.

• The second tier is targeted support for digital public infrastructure, logistics, and manufacturing. Anchored by the Digital India programme’s original ₹1 lakh crore envelope, Aadhaar, UPI, and the broader India Stack are the demand-side rails that make every digital mission commercially relevant inside India first. PLI, Railways Electrification, Freight Corridors, Ports, and Airports are networking physical India for the benefit of emerging National Champions.

• The third tier is domain-specific frontier Missions. The India Semiconductor Mission, with a ₹76,000 crore outlay, has cleared ten projects across six states for combined investment commitments of ₹1.60 lakh crore. Micron’s assembly, test and packaging facility in Sanand was inaugurated on 28 February 2026. The Tata Electronics-Powerchip fab at Dholera, with ₹91,000 crore in committed investment, targets first silicon by late 2026. Budget 2026-27 announced ISM 2.0 with focus on equipment, materials and design IP. The Comprehensive Nuclear Energy Mission for Viksit Bharat, with a ₹20,000 crore outlay, is anchored by the SHANTI Act passed on 18 December 2025, which opens nuclear power to private operators for the first time since 1962. The National Green Hydrogen Mission, at ₹19,744 crore, has allocated 862,000 tonnes per annum of green hydrogen production capacity to 19 firms and 3,000 MW of annual electrolyser manufacturing to 15 firms. The IndiaAI Mission, with a ₹10,372 crore corpus, has crossed 34,000 GPUs of public compute. Four sovereign foundation model builders have been selected. The National Quantum Mission at ₹6,003 crore is deployed across four Thematic Hubs at IISc Bengaluru, IIT Madras, IIT Bombay and IIT Delhi. The National Deep Tech Fund of Funds tranche at ₹10,000 crore, BioE3 at ₹10,000 crore, the National Supercomputing Mission at ₹4,500 crore and the National Mission on Interdisciplinary Cyber-Physical Systems at ₹3,660 crore complete the third tier.

The pattern is clear. Patient R&D capital at the bottom. Domain-specific frontier funding at the top. DPI and physical infrastructure in the middle. This is the emerging foundation.

The Market Geometry Is Already Reshaping

The combined effect of the two structural shifts is observable in private market traction across three patterns. We see this deployed across the 3one4 Capital portfolio in real time.

India Is Becoming a Trusted Global Supply Chain Node

The reshoring premium has stopped being a thesis and become a recorded balance sheet item. Apple assembled approximately 55 million iPhones in India in 2025, representing 25% of its global output of 220 to 230 million units, up 53% year-on-year. Indian iPhone exports crossed $10 billion in the first half of FY26. TDK has launched a state-of-the-art Advanced Lithium-ion Battery Plant in Haryana to manufacture 200 million battery packs annually, potentially meeting 40% of India’s requirement at full utilisation. Tata Electronics scaled its workforce to roughly 75,000 employees from approximately 15,000 two years ago, surpassing Foxconn’s India headcount across its Hosur facility and the acquired Wistron and Pegatron operations. India now hosts 2,117 Global Capability Centres employing 2.5 million professionals and generating $98.4 billion in revenue, with Bengaluru and Hyderabad as anchor locations.

Our thesis in action tracks the same shift. Scimplify closed a $40 million Series B in March 2025 to scale a specialty chemicals IP and manufacturing platform that now operates a network of over 200 production sites across India and exports to 16 countries. Pulse, launched in 2025 from Bengaluru, is building Made-in-India medical devices across infusion, critical care, cardiology, anaesthesia, renal care and diagnostics, anchored in the Make in India MedTech opportunity that earlier import duty structures had suppressed. Both companies are building for the FTA architecture while simultaneously serving the local geography.

Strategic Technology Moats Are Forming in Domains That Were Previously Uninvestible

The mission stack has shifted the risk profile of deep technology allocations in India. The demand is for companies that translate technical breakthroughs into scalable products and services, combining engineering depth with focused go-to-market execution. Private equity and grant capital can now underwrite decadal horizons in semiconductors, hardware-aware AI, advanced manufacturing, space tech, and robotics because the State has committed to building the factor conditions in parallel.

AGNIT Semiconductors, an IISc spinout, is scaling Gallium Nitride wafer and RF device production from Bengaluru. Its first international wafer exports are complete. Three RF products are in pilot trials with Indian strategic platforms. AGNIT is the first vertically integrated GaN semiconductor platform in India. Fermbox Bio is programming microorganisms into "micro-factories" that produce bio-based enzymes through precision fermentation. Their EN3ZYME product converts agricultural waste (bagasse, corn stover) into feedstock for 2G ethanol production at scale. Unbox Robotics is scaling AI-powered swarm intelligence robots for parcel sorting. Their UnboxSort system uses modular 3D robotic sortation with proprietary algorithms, delivering 50-80% space reduction and 3x productivity vs traditional systems.

This is the kind of domain-specific deep tech moat that the National Deep Tech Fund of Funds and the ISM ecosystem together are designed to enable. India’s specialty chemicals and CDMO base has been strengthening for a decade. The mission architecture now extends that proven IP-led playbook into semiconductors, synthetic biology, and physical AI.

The Sovereign AI and Energy Stacks Are Being Rewired in Parallel

Two of the most capital-intensive technology transitions of this decade are now backed by mission-grade State support and dedicated regulatory architecture in India. The IndiaAI Mission has crossed 34,000 GPUs of public compute, selected startups to build sovereign foundation models, and pushed Bhashini’s translation platform to over 300 million monthly translations across regional languages.

Hyperscale cloud and AI infrastructure has followed. Microsoft committed $17.5 billion to India in December 2025, on top of the $3 billion pledged in January 2025. AWS has committed $12.7 billion by 2030, on top of $3.7 billion already invested. Google announced a $15 billion AI hub in Visakhapatnam with Adani, which has separately committed $100 billion to AI data centre buildout by 2035. The Summit also produced the right kind of business-to-business announcements. TCS HyperVault will host OpenAI's Stargate workloads in India, starting at 100 MW and scaling to 1 GW. Infosys will deploy Claude through its Topaz AI platform. India's installed data centre capacity is set to grow from 1.3 GW to 9 GW by 2030.

AI innovators in our portfolio are marshalling these resources to deliver applied AI rapidly. Smallest.ai, building foundational voice models from Bengaluru, now handles over a million inference calls for global enterprise customers including RingCentral, Paytm, and Truecaller. Dozee’s contactless patient monitoring system, deployed across Apollo, Wockhardt, and Sahyadri hospitals with FDA 510(k) and CE Mark clearances, is live on 15,000+ beds and has saved over 20,000 lives across three countries. Vertical AI is finding native Indian customers at scale. H2LooP, headquartered in Bengaluru, builds hardware-aware vertical AI models for safety-critical embedded systems across automotive, aerospace, strategic, and semiconductor industries. Its positioning around IP sovereignty and on-edge reliability fits a regulated industry stack that general-purpose LLMs cannot serve.

On energy, solar overtook hydro as India’s largest source of clean electricity in 2025, reaching 9.5% of generation. In 2014, India had 2.82 GW of installed solar capacity. By March 2026, it had 150 GW. That is a 5,200% increase in a decade. Power generation from coal fell by 3.3% in 2025. Per capita coal generation in India stands at around 1 MWh, only 40% of China's level at the same PPP-GDP (in 2012).

India is already generating more solar per person and far less coal-based electricity than China at a comparable economic level. The structural reasons are clear in hindsight: a services-heavy economy, a climate that demands cooling over heating, and solar technology arriving at commercial scale just as India's power demand was accelerating.

Nuclear energy, with its 24/7 baseload capability, negligible carbon footprint, and land efficiency ~20x of solar, is the natural complement to renewables. The SHANTI Act, passed in December 2025, opened nuclear power to private capital for the first time since 1962.

India's EV market crossed 2.3 million unit sales in 2025, with two-wheelers at 57% of new sales. EV penetration in the three-wheeler segment had already reached 54% in FY24, the highest globally. These segments account for the bulk of India's passenger transport fuel demand. Their electrification, running on domestically produced solar electricity, can lead to a direct plateauing of crude import volumes.

Exponent Energy, named a World Economic Forum Technology Pioneer in 2025, has deployed its 15-minute fast charging technology in over 2,100 commercial EVs and 150 plus charging stations. Their integrated energy stack (e^pack battery + e^pump charger + e^plug connector) solves EV range anxiety without expensive battery chemistry. Yulu turned EBITDA positive in 2024 and has crossed 2 billion green kilometres of cumulative rides serving quick commerce and hyperlocal services. Vidyut, building commercial EV financing and Battery-as-a-Service distribution across 30 plus cities, is the financing layer beneath the broader electric mobility transition, with OEM tie-ups across Mahindra, Tata, JSW MG, and Piaggio.

The sovereign stack is taking shape across energy, data centres, and applied AI.

Whole Chain Missions Are the Next Logical Policy Structures

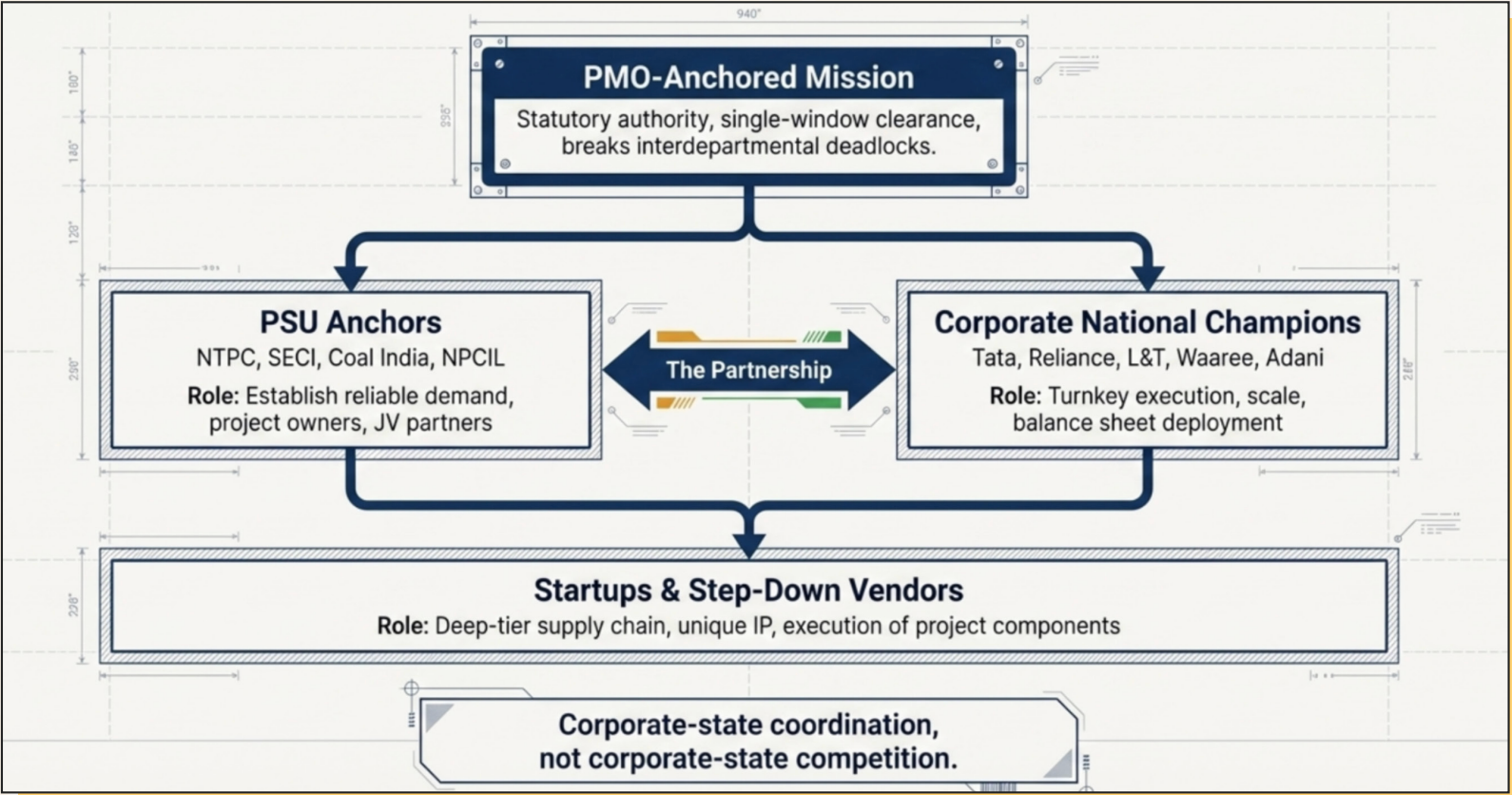

The mission stack is comprehensive, but implementation is key. The largest gap is one that the architecture has not yet been designed to close, and it now needs to be addressed by Whole Chain missions that would map every critical import dependency from mines to finished product across energy, fertilisers, rare earths, batteries, solar components, semiconductor materials and pharmaceutical APIs.

This Mission, led by a private sector leader of demonstrated capability, reporting directly to the Prime Minister's Office, with authority to cut across ministry boundaries, break interdepartmental deadlocks in real time, end nanny-state overregulation, and infuse cutting-edge market-aligned talent and competence into Mission implementation, must extend to 2047 and survive changes in government and commodity prices to deliver India's sovereign resilience through institutional design.

China holds an 85% share of India’s lithium-ion battery imports, supplies 90% of portable computers and 56% of imported solar cells to India. India's energy import profile is migrating from Middle Eastern oil to Chinese-dominated renewable energy supply chains. This is not diversification. It is the substitution of one concentrated vulnerability for another. The National Critical Mineral Mission and Rare Earth Corridors announced in Budget 2026-27 are useful starts but operate in isolation from energy and fertiliser planning. Individual ministries track individual commodities.

Until a single Mission owns the full picture from resource to finished product, India’s industrial policy is solving only the half of the problem it can see. The Whole Chain Mission is the next logical layer of the operating system.

China answered its structural problems with a specific institutional choice. It treated its largest corporations as instruments of national priorities. Solar, nuclear, coal-to-liquids, and EV manufacturing were each delivered through corporate champions operating under sustained state support and incentives. India will internalise these strategies.

The Whole Chain Mission can begin with a comprehensive vulnerability audit, then partner with private sector companies that have the capital and engineering capacity to execute projects for the PSUs. PSUs must be directed to distribute projects to National Champions, and this has already started. These Champions will each cultivate their own universe of step down vendors that execute components of each project. Startups can bring innovation and unique IP into these projects and build strategic partnerships with the Champions, eventually becoming Champions in their own domains. Just like DARPA initiated technologies that eventually led to the internet and GPS, entire ecosystems can be built under the irrigation of funding from each Mission and sector PSU.

India has done this before, in a different domain, at a scale almost no other country has matched. In 2010, India had enrolled zero people on Aadhaar. By 2016, more than a billion had completed onboarding. UIDAI was a focused authority with a single mandate, named leadership from the best of Indian industry, sustained PMO backing, convergent administrative coordination, and a delivery culture that absorbed resistance and converted it into infrastructure. The result was sovereign digital identity infrastructure built at population scale in compressed time with private sector partnerships.

The lesson is institutional. India can deliver mission-mode infrastructure when the architecture is right.

The State has now begun acting as a coordinated catalyst. The market geometry is shifting in response. As India climbs towards its $10 trillion GDP target, the work of the next decade is to launch these flywheels of innovation today.

Founders now have more opportunities to build full-stack National Champions, from IP and design to manufacturing and global GTM. An India on such a Mission will unleash its full potential for the prosperity of its citizens, and lend a new vibrancy to the technological transition underway globally.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)

-p-500.webp)

.jpg)