.webp)

Not Just Child’s Play: Inside India’s Fast-Evolving Parenting Market

India’s youngest citizens are rapidly becoming some of the country’s most influential consumers. As millennial and Gen Z parents seek to raise their children with style, comfort, and intentionality, spending across categories such as clothing, toys, wellness, and education is undergoing a significant transformation. No longer confined to functional purchases or generational hand-me-downs, India’s children’s economy now reflects a broader evolution in household consumption. Parents are investing in thoughtfully designed products, holistic learning tools, and opportunities for self-expression, often beginning before the child’s first birthday.

Whether through curated fashion, early learning programs, or digitally shared milestones, modern Indian households are showing a greater willingness to spend, provided the purchase aligns with trust, convenience, and aspiration. This shift is giving rise to a fast-evolving, premiumising “kidconomy” that offers brands a chance to build long-term affinity across emotional and lifecycle touchpoints.

Mini Shoppers, Major Market

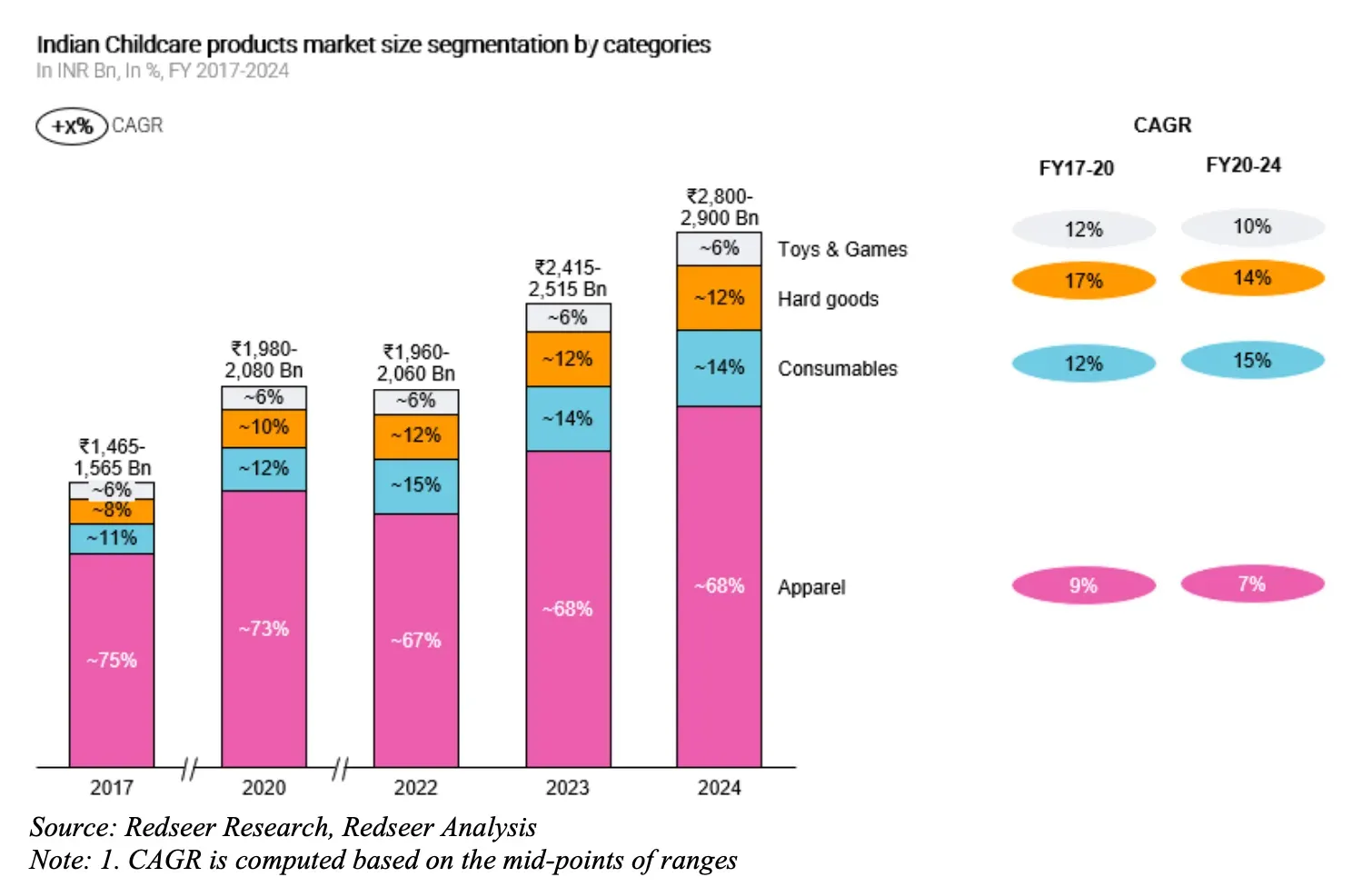

India has one of the highest birth rates globally, with 16.3 births per thousand people in 2022—approximately 1.5 times higher than that of developed economies. The country’s children’s products market, which includes fashion, toys, baby care, learning, and healthcare, is estimated at over ₹1.5 trillion and growing at a rate of 12 to 15 percent annually. Clothing alone accounts for nearly 30 percent of this figure, driven by increased disposable income and the rise of urban nuclear families. Platforms like FirstCry, Hopscotch, and emerging D2C brands such as Includ, Kidbea, and SuperBottoms are reshaping how Indian parents shop.

What was once an offline, price-sensitive segment has evolved into one powered by digital discovery, personalised shopping, and premium offerings. Although spending on childcare products remains relatively nascent, it is projected to grow faster than in many global markets. Apparel is currently the largest segment, accounting for 68 percent of the childcare products market in FY24. The Indian children’s fashion market is projected to reach approximately USD 22 billion by FY26, with the online segment expected to grow at a compound annual growth rate of 35 percent.

Spending is particularly concentrated among children aged four and below, who represented around 41 percent of the childcare products market in FY24—a figure that is expected to inch up to 42 percent by FY29.

Decoding the Spends of the “Kidconomy”

0–2 Years: The Essentials Phase Annual average spend: ₹30,000–₹60,000 per child

This phase focuses on essentials such as diapers, skincare, feeding gear, cribs, and strollers. These products account for nearly half of the ₹10 billion baby care and infant goods market in India.

2–5 Years: Discovery & Identity Phase Annual average spend: ₹40,000–₹75,000 per child

As children enter school and interact socially, discretionary spending on apparel, toys, and creative kits rises. Product trends include themed fashion, branded school accessories, and educational toys.

6–10 Years: Early Independence Phase Annual average spend: ₹60,000–₹1,20,000 per child

Parents begin investing in enrichment tools such as coding programs, language learning, Olympiads, and STEM kits. Wardrobe turnover also accelerates during this stage.

11–14 Years: Tween & Transition Phase Annual average spend: ₹80,000–₹1,50,000 per child

This stage sees a spike in spends on branded clothing, footwear, tech devices, and hobby-based accessories, with children beginning to influence purchase decisions directly.

So, What Changed?

The Rise of Millennial and Gen Z Parents India’s median age is around 28, and over 30 million births occur annually. A large proportion of new parents today are under 35. These digitally native parents are three times more likely than earlier generations to conduct online research before purchasing parenting products.

Growing Affluence and Double-Income Households Urban nuclear families dominate India’s middle and upper-middle-income segments. Around 38 percent of urban households now have dual incomes, and India’s per capita income has crossed ₹1.97 lakh. Discretionary spending in households with children has grown at a CAGR of 13 to 15 percent over the past five years.

Digital-First Discovery and Influence More than 75 percent of Indian parents now rely on platforms like Instagram, YouTube, and influencer content to guide purchase decisions. Content-engaged parents purchase over twice as frequently as non-engaged users, as per FirstCry’s DRHP.

Aspirational, Experience-Centric Parenting There is growing interest in premium, non-essential categories such as organic baby skincare (growing at 21 percent CAGR), STEM toys (market size of ~₹7,500 Cr), and enrichment apps. Parents now view their children as curated extensions of lifestyle, not just dependents.

Category Expansion and Lifecycle Thinking The estimated lifetime value of a child as a consumer in urban India ranges from ₹6–8 lakhs over the first 12 to 14 years. Brands are increasingly designing age-segmented offerings and expanding from toddlerwear to tween apparel, as well as from generic toys to specialised learning platforms.

Key Opportunities in India’s Kidconomy

Brand-Led Children’s Apparel Across Lifecycle Segments Most players focus on infants and toddlers, leaving room for full-stack brands spanning newborn to tween demographics. Includ is one such example building content-rich, gender-inclusive offerings.

Omnichannel Brand Strategies Despite the digital shift, offline formats remain critical. Brands like R for Rabbit are leveraging pop-ups, retail collaborations, and physical stores to drive trust and lower customer acquisition costs.

Edutainment and Experience-Led Platforms Parents seek engaging, screen-light educational alternatives. Companies like PlayShifu combine IP, gamification, and pedagogy to deliver edutainment at scale.

Trust-First Parenting Ecosystems From food to skincare, distrust around quality and safety remains high. Slurrp Farm has successfully built a certification-forward brand amplified by authentic voices and community influencers.

What It Takes to Win in the Kidconomy

To succeed, brands must:

The brands that will lead India’s kidconomy will combine trust, aspiration, and lifecycle depth. Success will come not just from selling what parents need but from shaping how they discover, share, and grow with their children. The next FirstCry, Patagonia Kids, or Carter’s equivalent in India will emerge at the confluence of design, empathy, and operational excellence.

.jpg)

-p-500.webp)

.jpg)