The Carbon Credit Market: Path to Net-Zero

Market Overview

Each year, the world emits approximately 51 billion tons of greenhouse gases into the atmosphere. To mitigate and prevent the impacts of climate change, we must reduce this to zero (net-zero) by 2050. Deeply embedded in industrial and production processes, these emissions are pervasive and reducing them poses a significant challenge. It will require concerted efforts from both the public and private sectors to overcome this global issue effectively.

Under the 2015 Paris Agreement, nearly 200 countries have endorsed the global goal of limiting the rise in average temperatures to 2.0 degrees Celsius above preindustrial levels, and ideally 1.5 degrees. Achieving the 1.5-degree warming target necessitates cutting global greenhouse gas emissions by 50% from current levels by 2030 and achieving net-zero by 2050. Reflecting this urgency, corporate alignment with climate goals is rapidly increasing: the number of companies committing to net-zero emissions has surged, doubling from 500 in 2019 to over 1,000 in 2020.

Companies are realising the need to go net-zero and must work towards decarbonizing their supply chains. They have to invest in both reduction and offsetting.

Challenges with Reduction

To achieve the global net-zero target, companies would need to reduce their emissions significantly (this also includes measuring and reporting the reduction, transparency will be key in achieving this and increasingly stakeholders are also getting interested in these parameters).

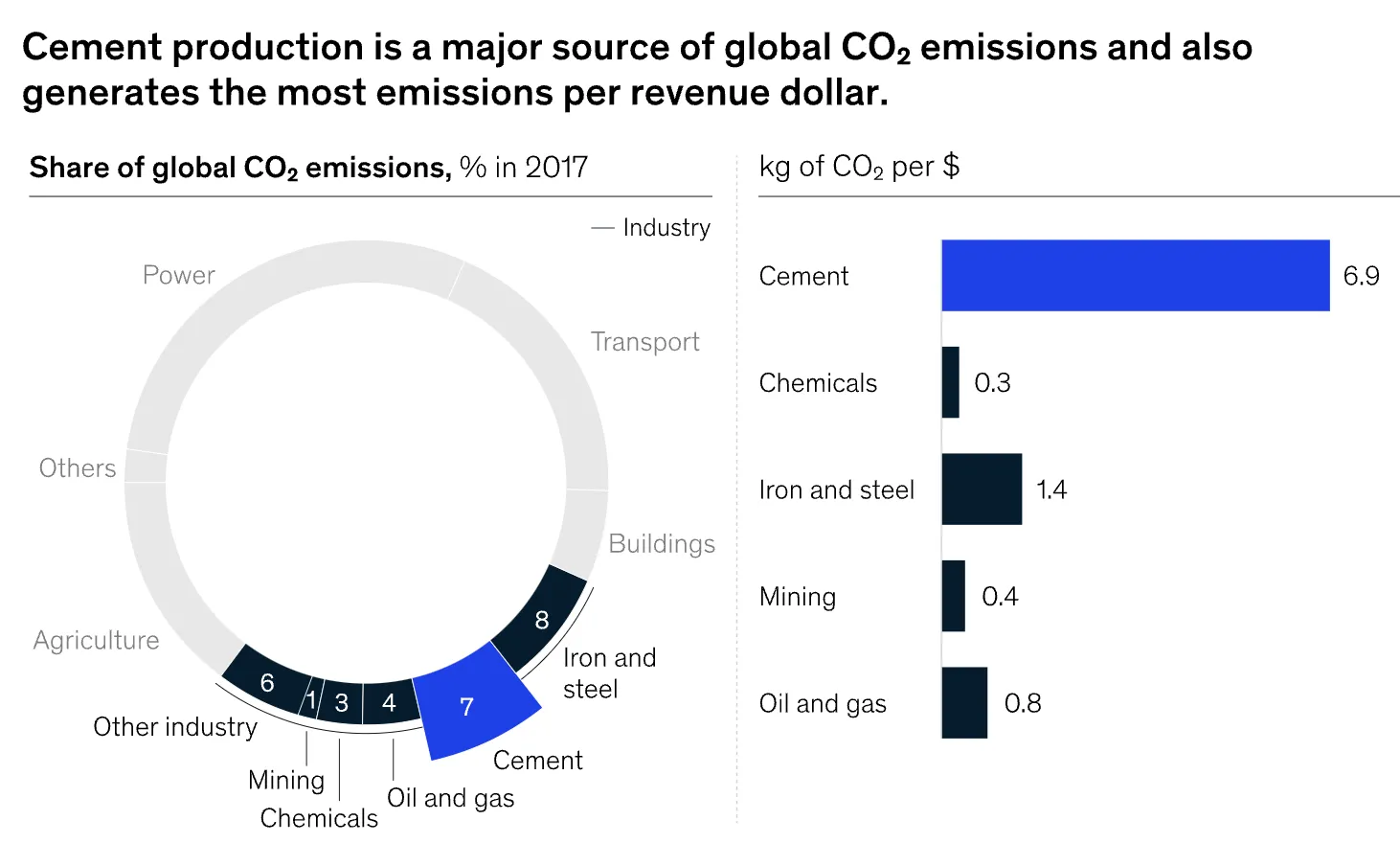

Even with all the reduction efforts, it’s extremely expensive to cut emissions completely for some companies. There are fundamental factors like the commercial viability of today’s available technology, expensive resources and certain processes that can’t be done with reduction. Cement production is responsible for 8% of global carbon emissions, largely due to the inherent chemical reactions and calcination involved in the process. This makes reducing emissions within the cement manufacturing process particularly challenging.

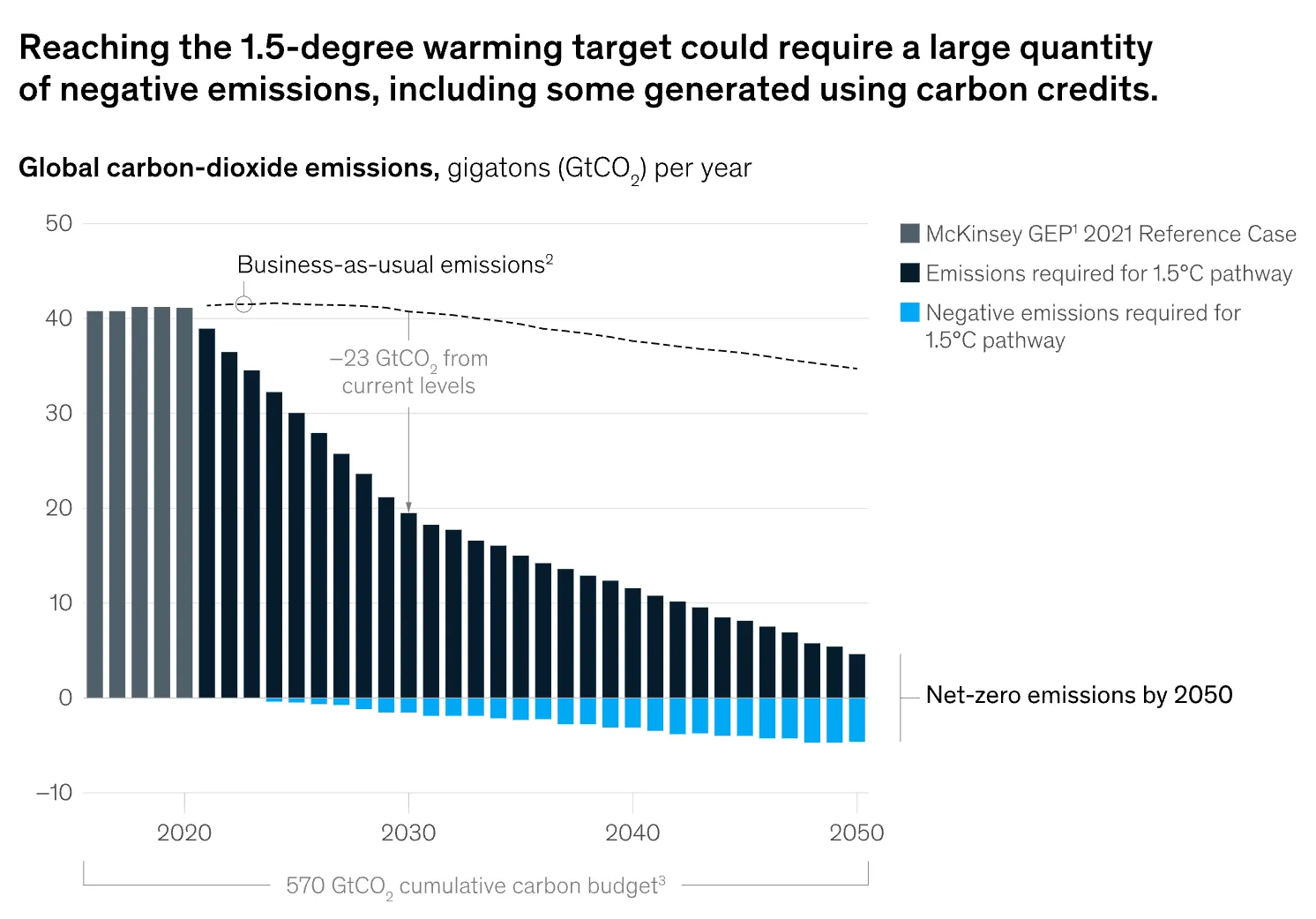

Due to these barriers, the emissions-reduction pathway to a 1.5-degree warming target essentially requires “negative emissions,” which are achieved by removing greenhouse gases from the atmosphere.

Offsetting

Given the difficulty, expense, and time required for reduction, carbon offsetting emerges as a practical alternative for organisations. As awareness of its benefits grows, an increasing number of companies are turning to the purchase of carbon credits as an effective way to address their emissions challenges.

Carbon credits are certificates representing quantities of greenhouse gases that have been kept out of the air or removed from it. While carbon credits have been in use for decades, the voluntary market for carbon credits has grown significantly in recent years.

A robust voluntary carbon market is one important tool the private sector can use to address climate change and reach net-zero emissions by 2050. This market is not just important for generating and offsetting through credits but also helps drive investments towards green technologies which otherwise would have been difficult to commercialise and wouldn’t have attracted investments.

If we don’t start financing innovation now, it will be impossible to reach our decarbonisation goals before we run out of time - Bill Gates

Market Size of Carbon Credits

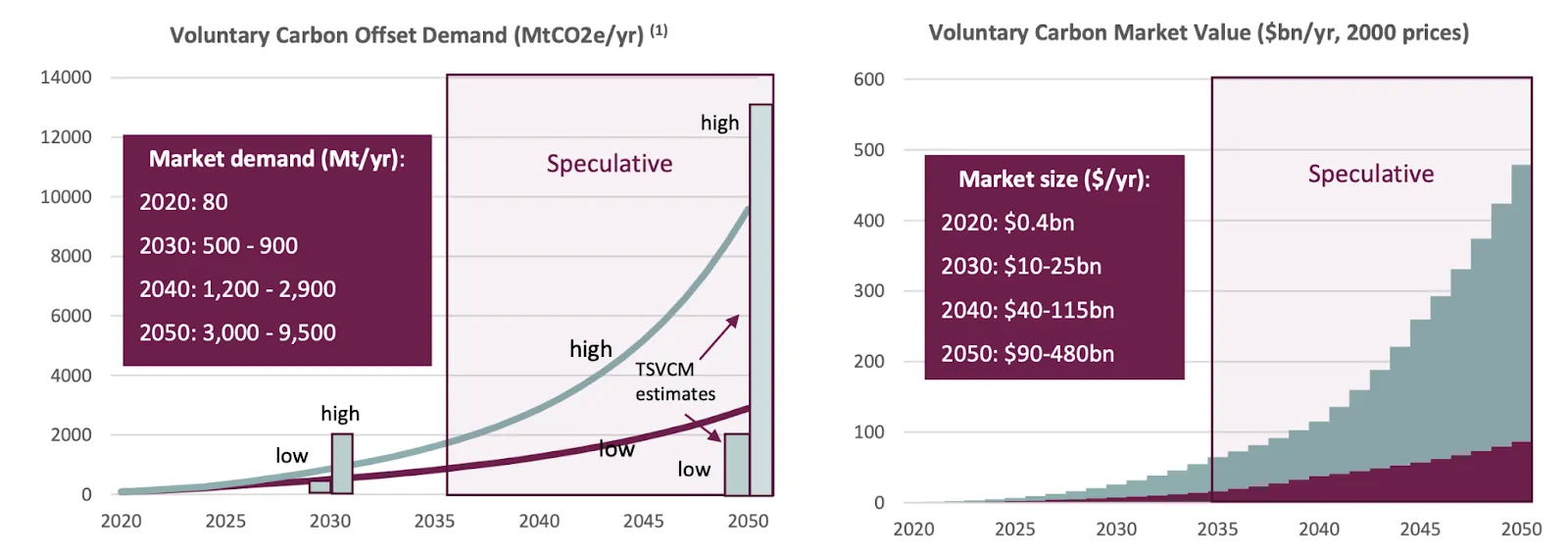

Based on different pricing scenarios and key market drivers, the carbon credits market could range from $5 billion to $30 billion by 2030 at the lower end, potentially exceeding $50 billion if market conditions are favorable.

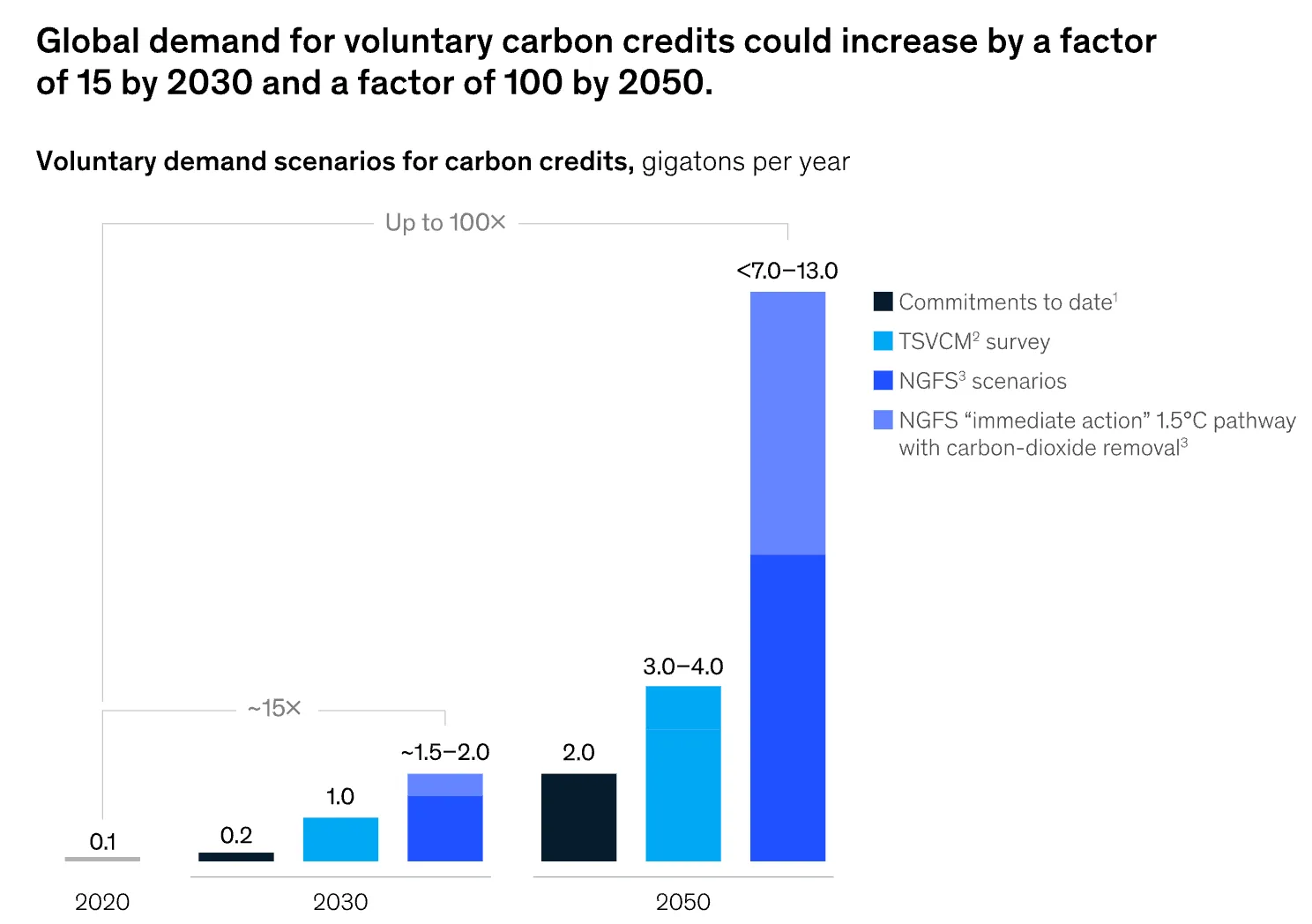

The Taskforce on Scaling Voluntary Carbon Markets (TSVCM), sponsored by the Institute of International Finance (IIF), estimates that demand for carbon credits could increase by a factor of 15 or more by 2030 and by a factor of up to 100 by 2050. Overall, the market for carbon credits could be worth upward of $50 billion in 2030.

The market for carbon credits purchased voluntarily (rather than for compliance purposes) is important for other reasons, too. Voluntary carbon credits direct private financing to climate-action projects that would not otherwise get off the ground. These projects can have additional benefits such as biodiversity protection, pollution prevention, public-health improvements, and job creation. Carbon credits also support investment into the innovation required to lower the cost of emerging climate technologies. And scaled-up, voluntary carbon markets would facilitate the mobilisation of capital to the Global South, where there is the most potential for economical nature-based emissions-reduction projects.

As efforts to decarbonise the global economy increase, demand for voluntary carbon credits could continue to rise. Based on stated demand for carbon credits, demand projections from experts surveyed by the TSVCM, and the volume of negative emissions needed to reduce emissions in line with the 1.5-degree warming goal, McKinsey estimates that annual global demand for carbon credits could reach up to 1.5 to 2.0 gigatons of carbon dioxide (GtCO2) by 2030 and up to 7 to 13 GtCO2 by 2050

Why is Supply so Difficult?

The existing projects in the market are insufficient to meet the escalating demand for credits, which is increasing rapidly. Moreover, most of these projects focus on nature-based sequestration and are limited to a few countries.

Another big problem with the existing supply is the problem of quality. Buyers pay a lot of attention to the quality of credits, and this is one of the most important factors in determining the price of each credit.

High-quality carbon credits are scarce because accounting and verification methodologies vary and because credits’ co-benefits (such as community economic development and biodiversity protection) are seldom well defined. When verifying the quality of new credits—an important step in maintaining the market’s integrity—suppliers endure long lead times.

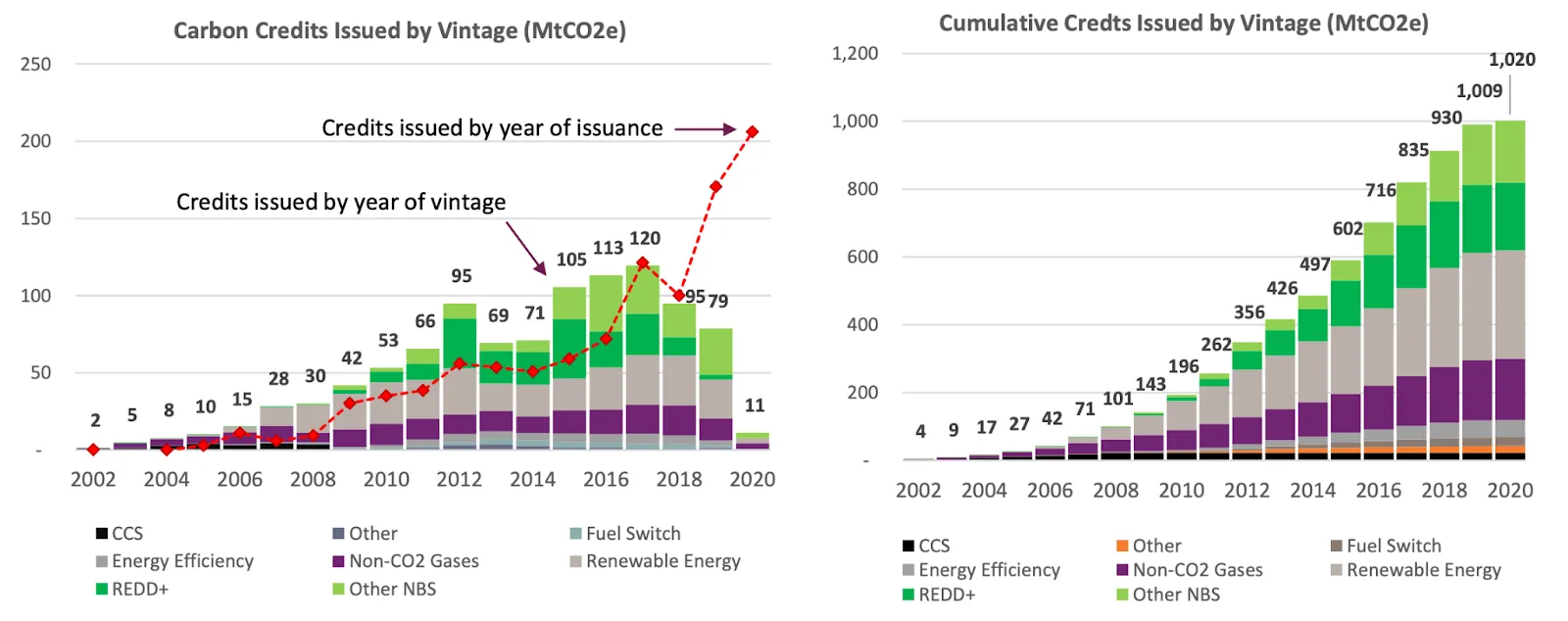

20% of these issued credits are from avoided deforestation (REDD+) projects, and another 18% from other Nature Based Solutions (NBS - including afforestation and agriculture). Together REDD+ and NBS account for nearly 40% of issued credits. Around a third of issued credits are from renewable energy projects such as onshore wind and solar installations. The left hand chart below shows credit issuances by year (red diamonds) and vintage (bars). Issuances have increased every year, with the exception of 2018. Issuances by vintage appear to decline in 2018, 2019 and 2020, but this is because issuances are often back-dated, ie credits issued in 2020 are for vintages in earlier years.

Even with all the projects under development, there still remains a very large opportunity to work on a diverse profile of creation projects and build a deep supply funnel of high quality credits. This has to be an approach where technology is used to its core and costs are uniquely controlled to build a business here.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)