Interplay of Tech and Capital in the Evolving Landscape of Insurance Investments

The Shift Toward Technological Advancements

Private equity firms and various other sources of private capital have been actively seeking new avenues to expand their asset portfolios and increase their AUM. In recent times, the insurance industry has garnered notable attention from investors, as its traditional business models undergo a substantial shift driven by technological advancements with a strong focus on enhancing customer experience.

This shift isn't merely operational—it's reshaping how insurance solutions are accessed and engaged with, resulting in a more customer-centric paradigm shift.

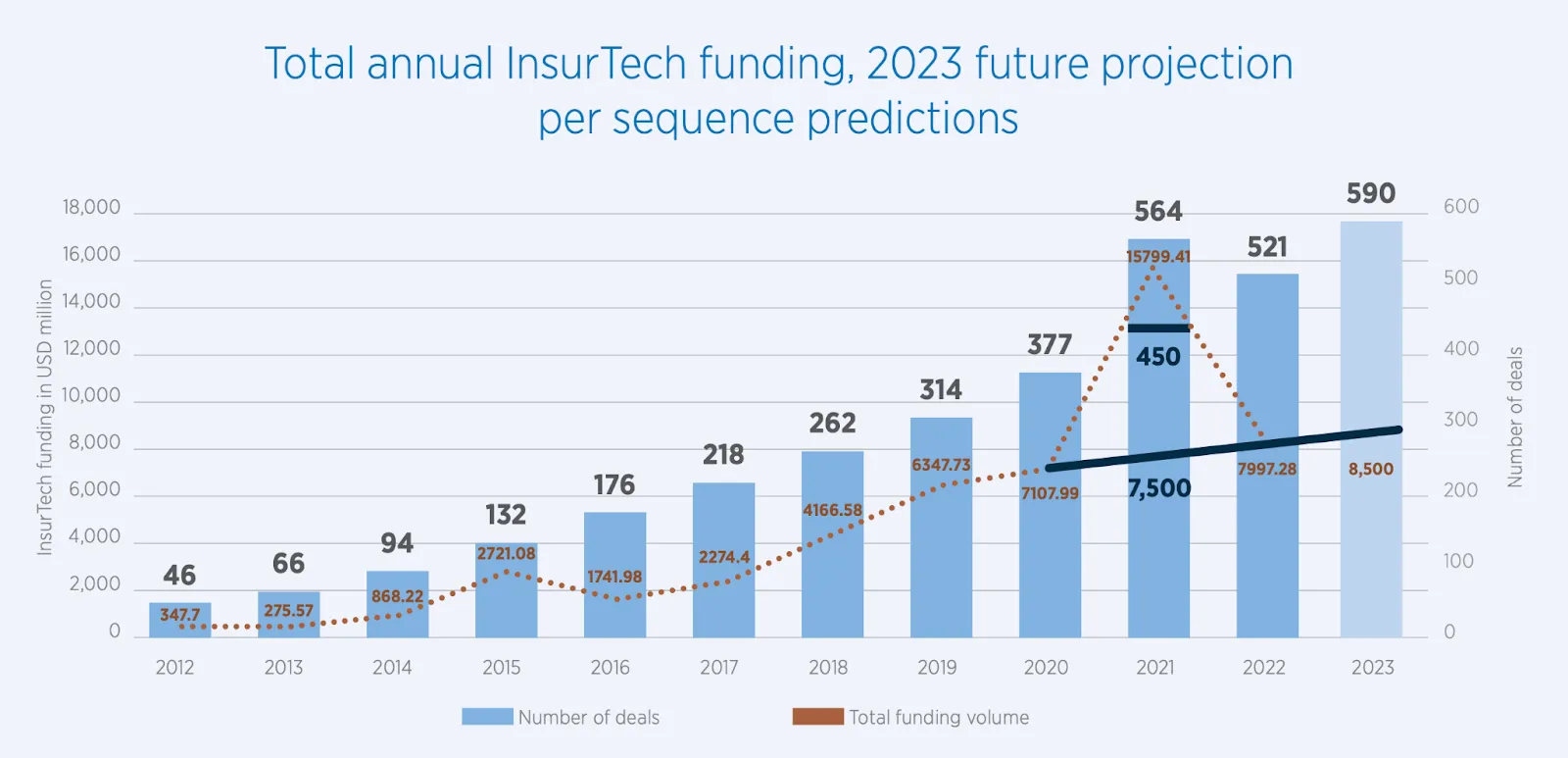

Analysing investment trends in the InsurTech(insurance technology) landscape provides a glimpse into the changing dynamics of the industry. While 2021 was marked by a surge in funding, it's crucial to consider this as an anomaly within the context of data from preceding years (Fig. below). Running projections based on historical patterns indicates a more accurate prediction of the number of deals and total investment. Despite the anomaly in 2021, the actual figures in 2022 (521 deals, and $7.9B) closely align with the projected numbers (515 deals and $8.1B), suggesting that the industry's growth trajectory remains consistent and robust.

Funding for InsurTech experienced a remarkable 37.6% QoQ (quarter-on-quarter) increase, reaching $1.39B. Even though the deal count remained stable, the average deal size grew by 25.3% QoQ, indicative of the industry's attractiveness for larger investments.

Asia Health Insurance Market

In Asia, limited coverage from universal health care schemes and rising consumer demand for better-quality care drive substantial out-of-pocket healthcare spending. Consequently, there is a significant increase in the demand for health insurance (Fig below)

The drive to mitigate economic uncertainties in healthcare has fueled a surge in the popularity of health insurance policies across the region. A noteworthy example of this trend can be observed in India’s growing insurance market, projected to reach $222B by 2026. With an average annual premium growth rate of 11.3% between 2013-14 and 2021-22, India is poised to become the sixth-largest insurance market globally, within a decade, surpassing the positions of Germany, Canada, Italy and South Korea. As insurers in India adapt to evolving trends, they are moving towards consistent profitability. The online distribution channel is gaining traction, and innovative business models are emerging around it. The IPO of Life Insurance Corporation (LIC) of India, the largest in the nation's history and the sixth-largest globally in 2022, further highlights the industry's significance. Monthly data from the Life Insurance Council reveals a YoY (year-on-year) growth of 9% in the overall APE (annualised premium equivalent), indicating a healthy trajectory.

“For social upliftment we believe the government should utilise the power of creating a regulatory framework for the private sector to innovate, take risks and deliver rather than spending the money directly. If 100 million middle-class families contribute Rs 10,000 per year as the health insurance premium, Rs 1 lakh crore can be raised which is more than the health budget of the government.”- Devi Shetty, Chairman & Executive Director, Narayana Health

Unveiling Trends and Insights in the Health Insurance Landscape

The InsurTech industry is in the midst of a transformation, particularly evident when examined in the context of global public markets. The convergence of factors such as consolidation, digitisation, and specialisation is moulding the trajectory of the health insurance and benefits sector. These trends are not only influencing investment decisions but also shaping the creation of value in a post-pandemic era.

Trend 1

Specialisation and Integration: Solutions Shifting from Sole Payer to Collaborative Partner

Publicly traded companies are undergoing a significant shift, moving away from their traditional roles as healthcare payers to adopt a more encompassing role as partners in healthcare services. Their strategic focus now includes preventive care, wellness programs, and value-added services, all aimed at enhancing overall health outcomes.

1. UnitedHealth Group (NYSE:UNH): A frontrunner in this transformation, UnitedHealth Group operates UnitedHealthcare, a major health insurer in the U.S. Their expansion into the Optum health services division has yielded impressive results with OptumHealth revenue per served consumer witnessing a remarkable 33% surge compared to the previous year. This growth was further bolstered by robust expansion in catering to new clientele and the remarkable performance across various sectors including home delivery, speciality, infusion, and community-based pharmacy offerings. Highlighting their dedication to promoting value-based healthcare solutions, UnitedHealth Group's strategic acquisitions, including the recent purchase of home health firm LHC Group for $5.4 billion, as well as the forthcoming acquisition of home and hospice care provider Amedisys for $3.3 billion, further emphasize their proactive approach.

2. Elevance Health (NYSE: ELV): Elevance (formerly Anthem), is actively investing in projects like managing pharmacy benefits with IngenioRxand strategic collaborations with healthcare providers. Their main goal is to offer comprehensive care solutions that enhance patient care coordination and health outcomes. The rebranding of Anthem to Elevance in June 2023 reflects their aspiration to go beyond the limits of a typical health insurance company and strive to be a lifelong partner in the health and wellness of its members. Elevance is also leveraging obstetric consultants and value-based incentive programs to positively impact maternal outcomes for Medicaid members.

3. Niva Bupa Health Insurance: Niva (formerly Max Bupa) is a joint venture between Max India (NSE: MAXIND) and Bupa. The insurer is making significant strides by customising health insurance plans that include offerings for senior citizens and products designed to support individuals managing chronic conditions like diabetes or hypertension. This well-thought-out strategy highlights a clear move towards specialised insurance products that address unique healthcare requirements.

Trend 2

Accelerated Digitisation - The Innovation Premium for Healthcare Insurance

Digital solutions are reshaping the healthcare insurance landscape, offering improved access to care, interventions at scale, and cost-effective avenues compared to traditional channels. These solutions facilitate data collection, allowing for highly personalised products. Through real-time underwriting decisions driven by automation and intelligence, this digitisation creates a competitive edge in rapidly evolving digital distribution channels. Innovations like quantum computing, 5G, large language models (LLMs), and virtual reality are accelerating this journey.

1. Cigna (NYSE: CI) - Cigna launched a new concierge care platform, Pathwell, that integrates Evernorth's data analytics, clinical expertise, and digital solutions with the medical benefits and network of the health plan. The primary goal is to offer personalised, comprehensive care experiences to members managing high-cost conditions such as oncology and kidney disease. Pathwell's initial focus is on patients with musculoskeletal conditions and those requiring injectable or infused biologic drugs.

2. CVS Health (NYSE: CVS) - CVS Health is doubling down on investments in the virtual care sector. It's taking the lead in fundraising rounds for virtual psychiatry and therapy practice (Array Behavioral Care) and for in-person and virtual healthcare companies (Carbon Health). Furthermore, CVS Health's Virtual Primary has extended its telehealth-based mental health care services, allowing individuals to schedule appointments with licensed therapists and psychiatrists.

3. Amplify Health - Amplify Health, a Singapore-based venture between AIA (HKG: 1299) and Discovery Group, has acquired AI solutions provider AiDA Technologies, enhancing its AI capabilities for underwriting, claims processing, and fraud detection. This acquisition complements their existing suite of solutions which include claims processing, administration systems, digital health programs for chronic disease management, and insurance product development.

4. Shriram Life Insurance (NSE: SHRIRAMFIN) - With about 45% of its retail premium stemming from rural areas, Shriram Life Insurance is leveraging AI and digital technology to optimise retail claims management. The company’s growth has been fueled by technology-driven sales strategies, prioritising seamless processes such as paperless proposals and eKYC for swift verification. Through AI-based predictive models, Shriram Life Insurance proactively anticipates claim trends, enabling timely and proactive service delivery to policyholders and nominees alike.

Trend 3

Consolidation and Industry Convergence

Anticipating a convergence of insurance and other sectors, the insurance landscape is evolving towards collaborations, mergers, and reimagined value propositions for customers. Insurers are collaborating with InsurTechs, healthcare providers, and non-traditional market participants to create new ecosystems and deliver enhanced products and services.

The digital health sector is moving from isolated solutions to integrated platform companies. This integration aligns with the primary offerings of these ecosystems.

1. Ecosystem Partnerships - Insurers are developing partnerships with non-traditional market players, InsurTechs, and healthcare providers to introduce new offerings, enter new markets, and boost engagement with policyholders. AXA Hong Kong and Macau, for instance, joined forces with CoverGo, a no-code insurance SaaS platform, to enhance their insurance ecosystem. By leveraging CoverGo's advanced technology, AXA aims to streamline customer experiences and accelerate time-to-market for general insurance products.

2. Converging Group and Individual Coverage - Emerging propositions are blurring the lines between group and individual coverage, offering consumers a balanced approach. Insurers are tapping into the employer channel to sell individual policies, engaging employees as an alternate distribution channel. Additionally, insurers are defining criteria to classify individuals into categories for hybrid plans that incorporate both personal preferences and collective underwriting. Canadian life insurance firm Sun Life Financial (NYSE:SLF) acquired Dialogue Health Technologies, a virtual health and employee wellness platform, for a total equity value of CAD 365 million. The transaction will empower clients with proactive health management at various stages of their well-being journey. Earlier in March 2020, Sun Life had rolled out Dialogue's services to its Group Benefits Clients under the name Lumino Health Virtual Care.

3. Digital Platforms and Marketplaces - The integration of digital platforms and online marketplaces is transforming how health insurance products and services are accessed, distributed, and managed. Regulatory authorities like the IRDAI emphasise the importance of intermediaries, driving the development of hybrid and specialised customer service platforms for purchasing insurance. This focus has led to the emergence of initiatives such as Bima Sugam, an online insurance marketplace, aimed at engaging all players in the industry. Companies like eHealth (US) and Policybazaar are notable examples of platforms that bring together multiple insurers, offering consumers a comprehensive range of health insurance options alongside value-added services.

Unlocking Capabilities for the Next Wave in Insurance

The evolving landscape of public markets is moulding trends in private investments, serving as catalysts for innovative breakthroughs in the Health Insurance market. These trends are redefining how insurance is experienced, offered, and integrated into our lives.

1. Value-based care models

The rise of value-based care models is driving changes in insurance offerings. Beyond traditional coverage, insurers are embracing a holistic approach by incorporating value-added services into policies. These services range from assisting with claims to including preventative measures such as early health screenings and mental health support. Companies bridging the gap between insurers and healthcare providers, particularly those enabling data exchange and health informatics, are poised for rapid growth. Notably, Urban Health, backed by 3one4 capital, is making strides in enhancing healthcare delivery to underserved communities, senior populations and Medicare Advantage population ushering in timely and improved healthcare. It is currently supercharging ROI with data-driven Care Management - helping primary care (providers, clinical staff and care team) lead the Value Based Care Charge.

2. Insurance for the blue economy

In 2022, 2 billion workers were informally employed worldwide according to the International Labour Organization. With a growing gig economy, the proliferation of contract and freelance workers has spurred demand for tailored insurance solutions. Insurance is shifting its focus to meet the unique needs of these informal workers.

Gig workers as proportion of global workforce (Source: Gartner) 2021: 15%-25% 2025: 35%-40%

Companies like Bestow are leveraging AI-powered underwriting to offer swift, no-examination term life insurance for small business employees and gig workers. As the gig economy continues to reshape the employment landscape, insurers are stepping up to provide essential coverage previously limited to traditional employer arrangements.

3. Embedded Insurance

By 2030, embedded insurance in Asia is expected to grow to become a $270 billion market in terms of GWP, according to McKinsey analysis. Embedded insurance is revolutionising the industry by seamlessly integrating insurance into various customer journeys. For instance, offering life insurance during the mortgage application process provides benefits such as lower acquisition costs, reduced volatility, and increased value for end customers. By leveraging digitization, advanced analytics, and design thinking, insurers can anticipate customer preferences and needs. The collaboration between Flipkart and Aegon in India exemplifies this trend by making life insurance accessible while applying for a mortgage, thereby improving affordability and flexibility.

4. AI to Power Up Insurance Models

The transformative potential of generative AI is reshaping every aspect of insurance, from underwriting and risk modelling to claims processing and customer services. AI's role in InsurTech is centred on enhancing customer engagement and streamlining operations. Advanced data analytics can provide deeper insights not just for generating and retargeting leads, but also for utilising these results in handling provider networks, claims, pricing, and risk management. AI can also be used to enhance customer service interaction by using chatbots as well as enhance operational efficiency through robotic process automation, claims adjudication, and predictive analytics. US-based Sproutt employs AI and proprietary analytics to provide personalised insights for agents and customers, leading to tailored life insurance solutions that align with individual needs.

5. Making Insurance Inclusive and Accessible in developing geographies:

Catering to the requirements of 300 million Indians in the middle-income bracket, who are unable to cover hospitalisation costs yet can manage reasonably priced health insurance, demands a transition from 'universal healthcare' to 'universal health insurance'.Most of IRDAI’s initiatives focus on deepening insurance penetration, which is currently at 4.2 per cent (premium to GDP). IRDAI is eyeing insurance penetration of 8-10 per cent by 2027. Initiatives like Bima Sugam and ABHA aim to make insurance and related services accessible to all. Eka Care, with over 30 million health records and 1.6 million ABHAs, has established itself as the largest repository of health records in India. Converting ABHA into a Health Savings Account supported by UPI can provide a digital method for storing medical records. Additionally, companies like WeRize have been providing tailored, affordable micro-insurance products, including coverage for diseases like dengue and malaria, to cater to low-income communities, gradually familiarising them with insurance.

6. Transforming Employee Health Insurance to Employee Well-being

Insurance companies are reshaping employee health insurance to encompass overall well-being, entering into fiercer competition with banks, wealth managers, and technology-driven startups. Employee benefits are evolving through broker platforms, offering comprehensive services and personalisation. PazCare, part of 3one4 capital’s portfolio, creates care ecosystems for employers, integrating health insurance with wellness solutions like tele-doctor consultations and mental health support. Its integrated approach also includes financial planning, tax benefits, and decision support tools.

As the insurance landscape evolves, these trends are poised to drive innovation, enhance accessibility, and provide more value for consumers across the globe.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)

-p-500.webp)

.jpg)