.webp)

India's Insect Protein Market

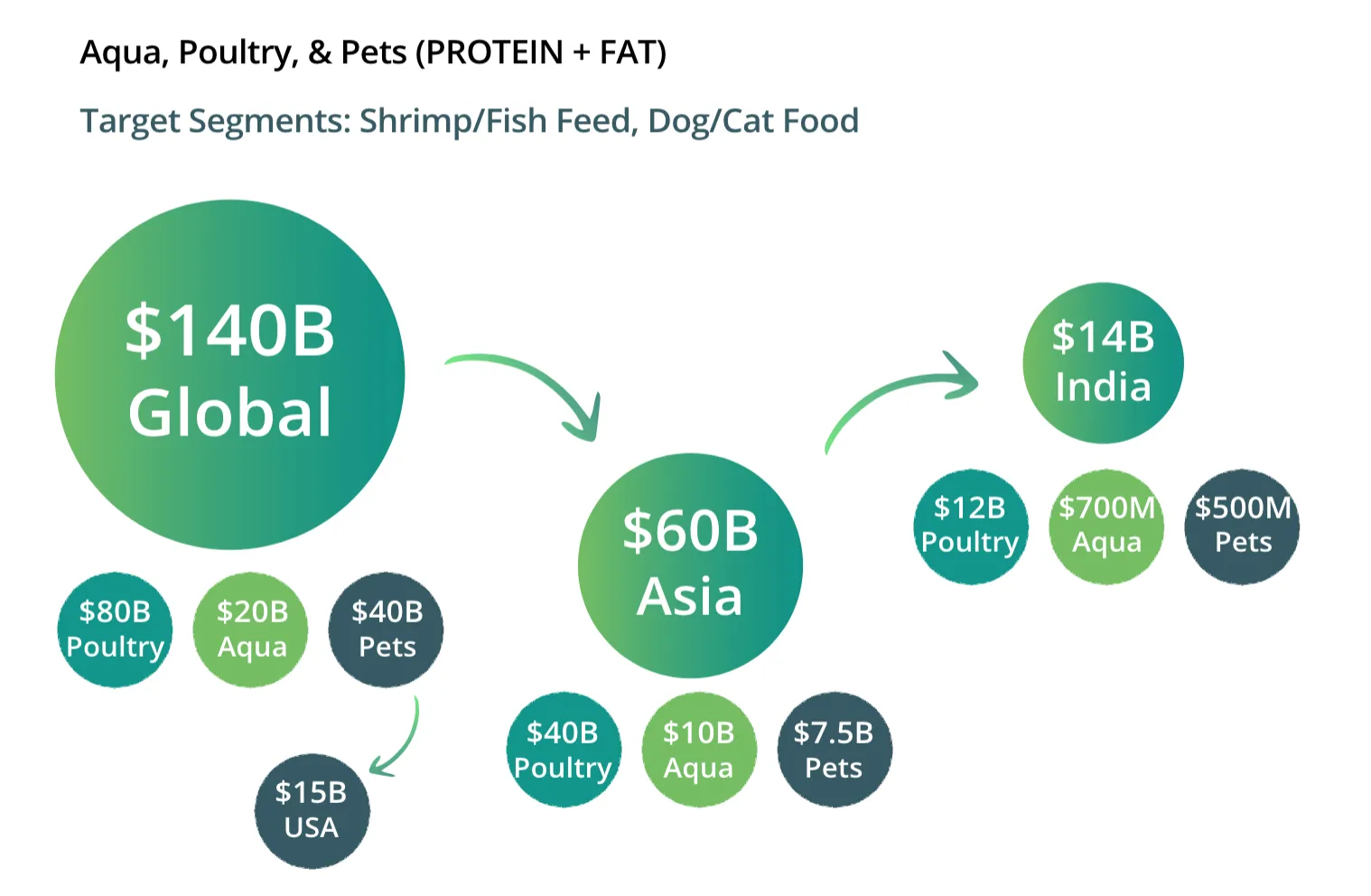

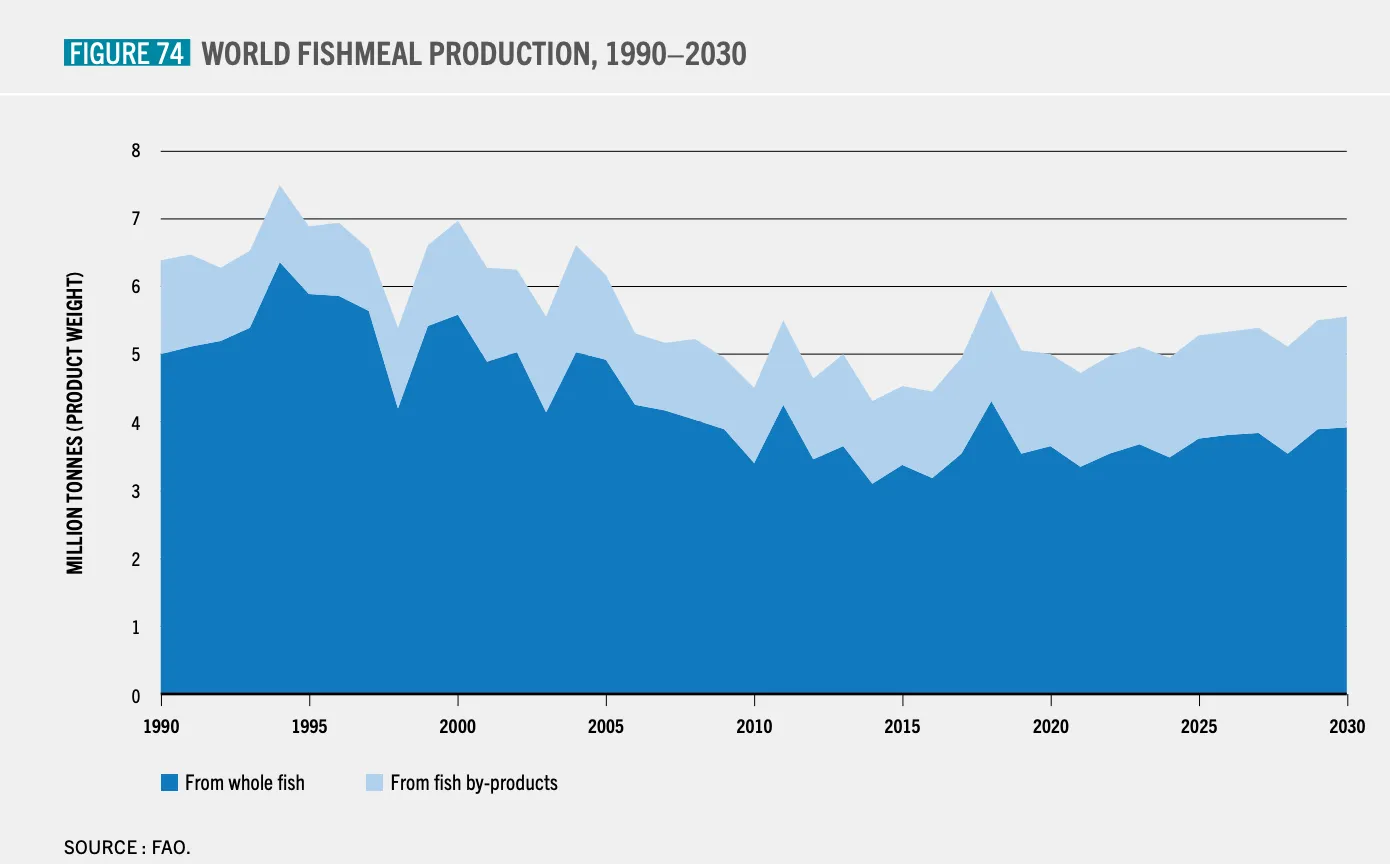

The demand for meat in India is expected to nearly double in the coming decades, presenting a significant challenge to the industry due to anticipated shortages in essential animal feed ingredients. Annually, millions of tons of wild fish, including sardines and anchovies, are harvested and transformed into fishmeal and fish oil to sustain farm-raised animals. According to the Food & Agriculture Organization (FAO), 50% of marine fish species are either fully or over-exploited, reflecting a critical sustainability issue. India, for instance, utilises 600,000 to 700,000 tons of wild-caught fish annually for animal feed production. This surging demand underscores the urgent need for alternative protein and oil sources beyond what current fishmeal and fish oil production can provide, pushing the aquaculture sector towards a tipping point.

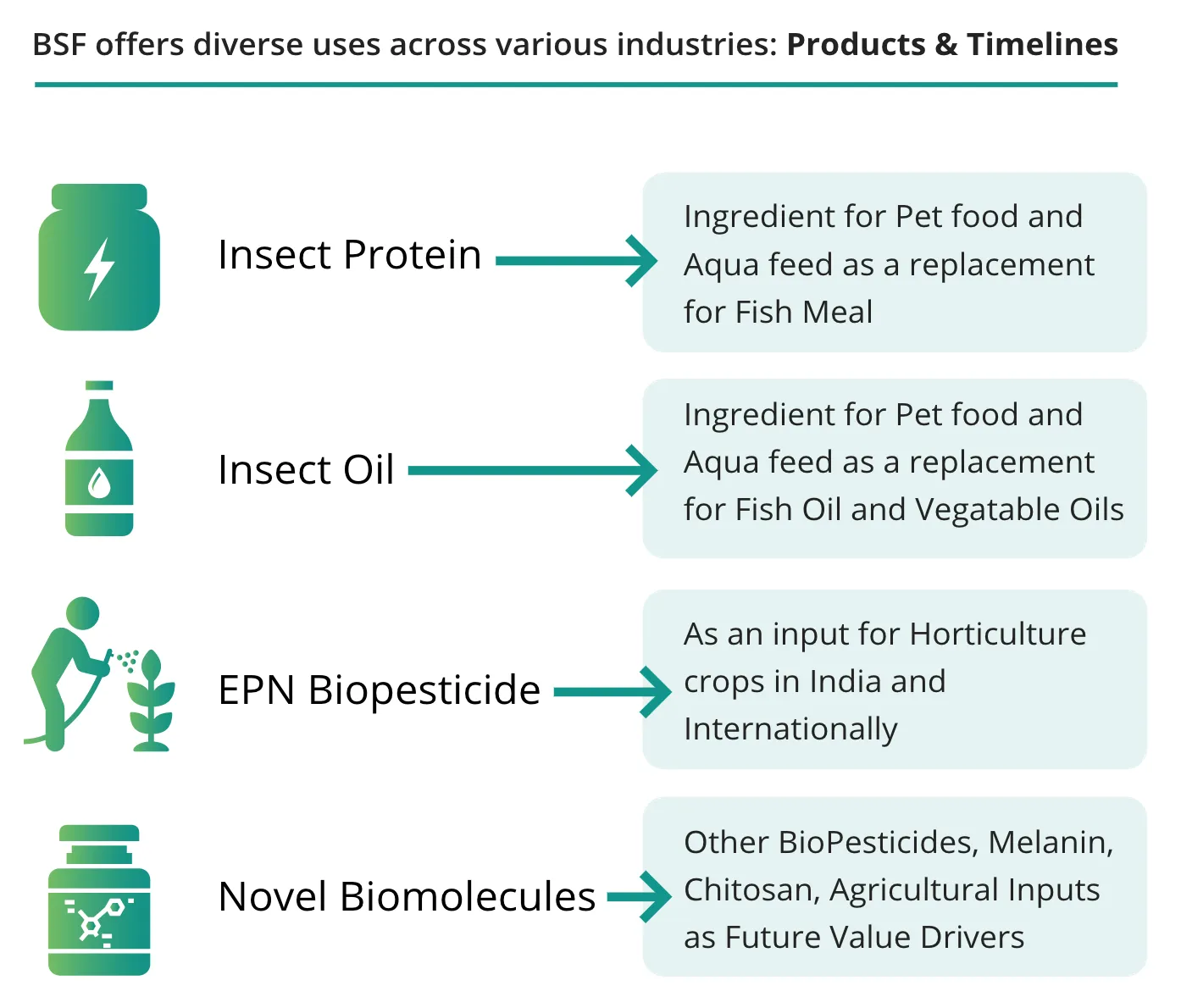

In response, feed manufacturers worldwide are exploring sustainable alternatives such as Black Soldier Fly, Silkworm, Crickets, and Grasshoppers for feed protein. These initiatives involve mass-producing insect larvae using by-products from the Food & Agriculture industry, aiming to create insect-based protein and oil for feeding shrimps, pigs, poultry, and pets. While Europe and Southeast Asia are seeing significant advancements in this arena, India stands on the brink of innovation, with the potential for breakthrough developments in sustainable feed production. This shift not only addresses the impending feed shortage but also aligns with global efforts towards more eco-friendly and sustainable agricultural practices.

Decrease in the Supply of Fish Meal from Oceans

Black Soldier Flies (BSF), being tropical insects, are capable of flourishing year-round, with their breeding particularly favoured in India's southern regions due to the warmer climate and plentiful sunlight. Although commercial production of BSF is viable in various climates, environments with temperatures falling below 10°C often require supplemental heating, highlighting a geographical advantage for India. This advantage plays a critical role in the cost disparity between BSF production in India and that in Europe or many parts of America. The necessity for additional heating, lighting, and sophisticated automation in cooler climates results in insect farming companies in Western countries incurring capital expenditures up to six times greater than those in India. Consequently, this leads to significantly higher operating costs for Western firms, emphasising the economic and environmental efficiencies of BSF production in warmer regions like India.

All international feed manufacturers have already tried BSF as an ingredient. The market is commoditised and dominated by legacy products with negligible innovation. Challenges to scale include:

- Rising Input Costs

BSF companies have successfully tackled the challenges associated with constructing the necessary engineering for scaling, utilising locally available feedstocks and substrates. These include brewers' spent, agriprocessing by-products, and palm by-products such as palm kernel expeller. However, with the growing scale of these companies, there has been an increased demand for these substrates, which are also utilised in other livestock industries like cattle and poultry. For instance, brewers' spent, now valued at 80-100 Euros per ton, has seen a significant shift from being discarded in landfills 5-7 years ago. The ban on rice bran exports in India has further influenced the price of palm kernel expeller due to heightened demand from the Australian cattle industry.

What initially began as zero-cost waste has now gained value, directly impacting the cost of Black Soldier Fly Larvae (BSFL) production. Another hurdle arises from substrates like brewer's spent not being considered waste in India, a country with the largest cattle and poultry population. For example, brewers' spent trades at Rs 9-10 per kg in India. If BSF is cultivated on brewers' spent, the Feed Conversion Ratio (FCR) is 4-5%. Consequently, the cost of BSF in India is 2-3 times higher compared to fishmeal. As more companies expand, the availability of substrates for rearing BSF is projected to become the primary limitation. Without differentiation and with BSF solely positioned as a fishmeal replacement, companies risk being perceived as commodities, hindering scaling efforts in the segment.

- Pricing

The key to success in the market lies in achieving the right price point, which, once attained, will drive scalability. The market potential is substantial, with India alone consuming 13 million tons of shrimp feed annually, and the demand is consistently increasing. A slight shift in replacing fish meal with BSFL could have a significant impact, given that the current shrimp feed uses approximately 200,000 tons of fish meal. However, the challenge remains in securing a sufficient supply of substrates.

Evaluating Silkworms as a Sustainable Feed Source

Alternatively, considering a multi-insect approach, silkworms appear as a viable option. Yet, the current supply of dry Silk Worm Pupae (SWP) is limited to 8,000-12,000 tonnes, significantly less than the 200,000 tonnes of fishmeal annually required for the shrimp industry alone. The potential Total Addressable Market (TAM) for SWP is confined to INR 100-120 crore, assuming a selling price of INR 100. However, manufacturing silkworm protein presents various challenges, including variable batches, contaminants in raw materials, and difficulties in separating fat due to the presence of silk fibres around the pupae.

Key to BSF Success

Therefore, success in this segment will be determined by companies focusing on BSF, and developing intellectual property to provide functional value beyond mere fishmeal replacement. This could involve delivering enhanced growth, reducing mortality due to diseases, and improving Feed Conversion Ratio (FCR) at a comparable price to fishmeal, ultimately leading to improved bottom-line performance and demonstrating a willingness to adopt these innovations.

BSF Go-to-Market Strategy for India's Feed Sector

In India, the feed manufacturing sector comprises numerous players, with the majority of the market share concentrated among the top 6-7 entities. However, customers perceive minimal differentiation among these brands, leading to farmers frequently switching between them. The key driver for farmers is the delivery of functional benefits that positively impact their bottom line. In this unregulated market, farmers harbour scepticism about product claims, emphasising the importance of scientific validation through extensive field trials and collaborations with reputable agencies such as CIBA to establish a unique identity in a crowded landscape.

Initial traction in this competitive market could be gained through influencers. Lead farmers in each district or Farmers Producer Organization (FPO) play a pivotal role as influencers. Collaborating with these influencers to showcase the Return on Investment (ROI) could generate a multiplier effect and build credibility.

However, distribution poses a challenge, given the intricate credit and financing cycles involved. A prudent approach at the early stages might involve partnering with an established feed manufacturer for sales and distribution or exploring potential collaborations with digital platforms.

The insect ingredient business is anticipated to become a commodity, demanding competitiveness with traditional feed ingredients and emphasising cost efficiency in large-scale production. To maintain a competitive edge, strategic investments in research and development, particularly in innovative feed formulations, are paramount. Staying ahead in BSF genetics and refining process engineering will be crucial for ensuring healthy profit margins. Therefore, success in this sector hinges on striking a balance between effective biology and process engineering.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)

-p-500.webp)

.jpg)