New Tidal Forces for the Indian Economy

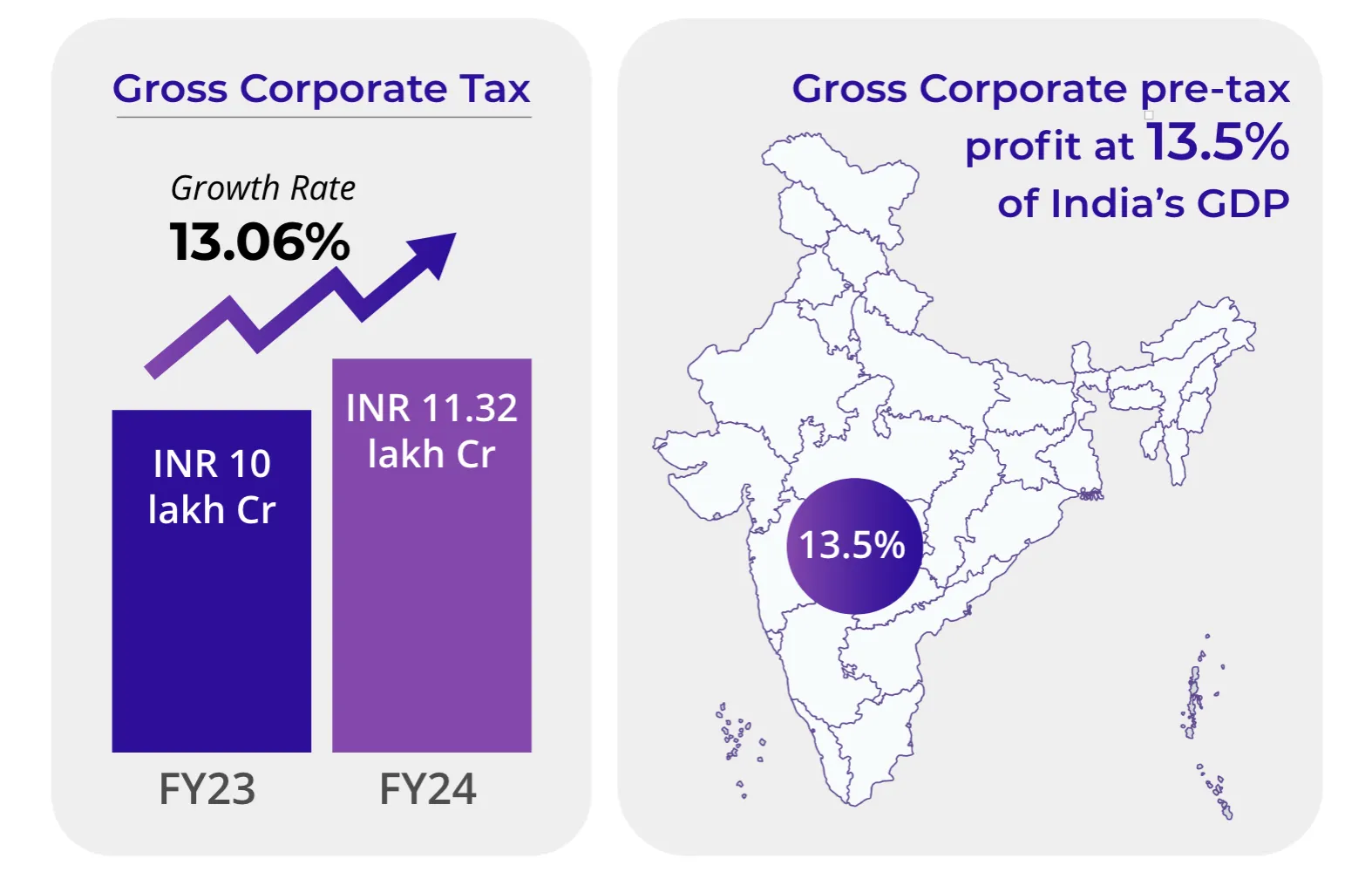

India Inc. Records Highest Profitability at 13.5% of India’s GDP

What does this mean for corporate growth strategy?

Encouraging Signs: India’s Gross Corporate Tax collection (provisional) in FY 2023-24 stands at INR 11.32 lakh crore, marking a significant growth of 13.06% over the INR 10 lakh crore collected last year.

Assuming the Gross Corporate Tax rate is 25%, India Inc. (listed and unlisted) has generated INR 45.28 lakh crore of pre-tax profits over FY24!

This is ~13.5% of India’s GDP as of March 2024.

This staggering statistic explains the tidal force underneath the Indian capex cycle underway. As India Inc. pays down its debts from its free cash flows, it is also allocating capital to new projects and aggressively expanding capacity. Bank borrowing from corporations has slowed down as companies invest in expansion from their earnings, leading to healthier balance sheets. The public markets are rapidly rerating several Indian companies as they demonstrate new strength in earnings growth, capital allocation, and strategic expansion.

Morgan Stanley reports that India's capital expenditure (capex) cycle is experiencing a resurgence, reminiscent of the growth seen during the 2003-2007 growth period. The analyst projects that by 2027, India's investment as a percentage of its gross domestic product (GDP) could reach 36%, fueled by public capital expenditures, increasing exports, and a stable economy. This mirrors the trend from 2003-2007, when the investment ratio in India peaked at 39%.

The analysts have noted that the current increase in investment growth is predominantly driven by public capex, in contrast to the previous cycle during 2003-07, which was led by private capex. They believe that the emphasis on public capex is crucial for the sustainability of the capex cycle, given the typically long gestation periods associated with infrastructure projects. As India Inc. sees higher profitability, an increase in private capex is anticipated, which could potentially elevate overall investment to target 40% of GDP.

India’s EoDB Transformation

Ease of Doing Business improvements are increasing the velocity of GDP growth

In the past decade from 2014 to 2024, India has taken its place as a Top 5 global economy, on track to soon place third behind only the US and China. This formidable trajectory also reflects in the remarkable leap forward in the nation’s Ease of Doing Business (EoDB) rank – from 142 in 2014 to 63rd in 2024.

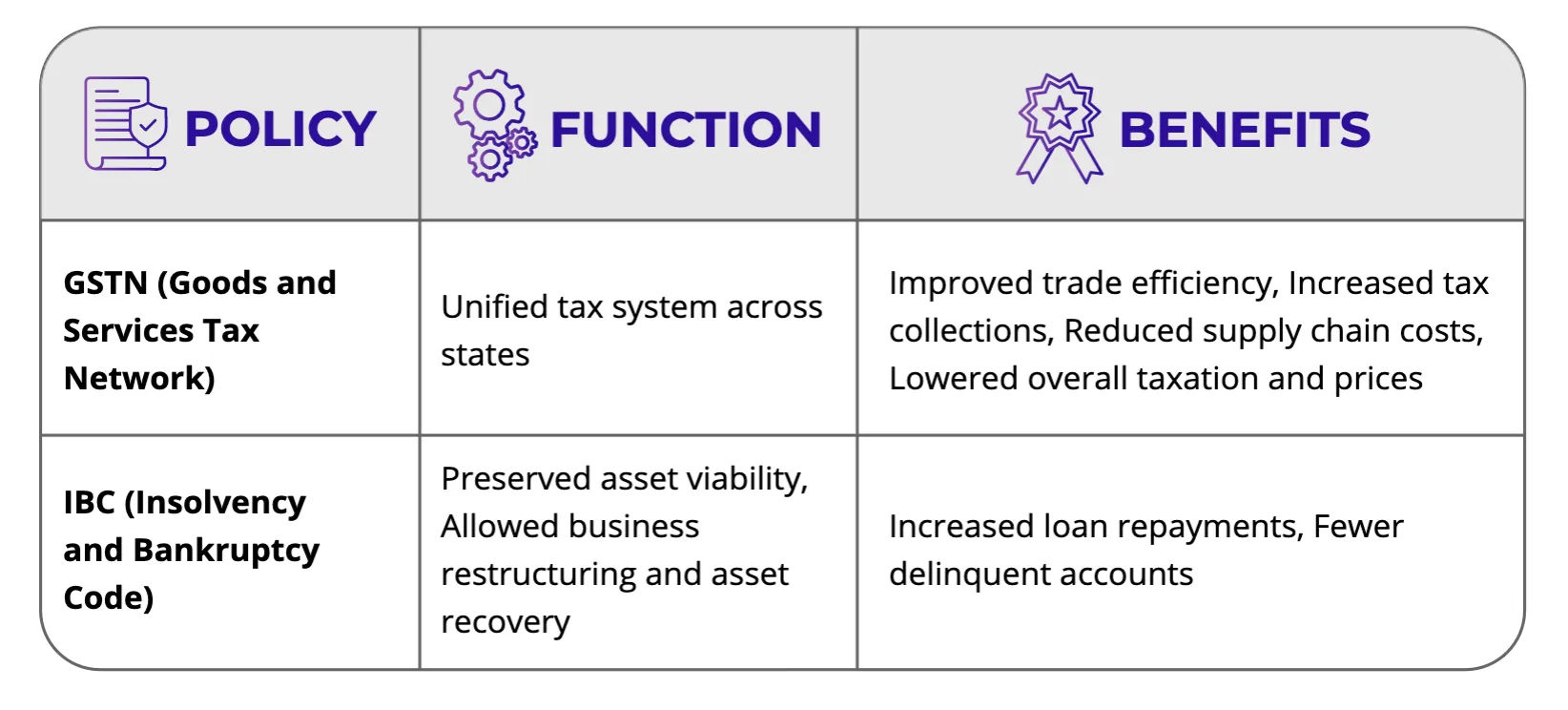

Numerous measures across multiple economic sectors have converged towards this favourable EoDB trajectory. The Goods and Services Tax Network (GSTN) unified the country’s states and UTs under one intra-national economic market system by integrating many fragmented tax systems. Heavily digitalized, the GSTN system has wielded multiple breakthroughs in making trade across the country more efficient, increasing tax collections, and decreasing supply chain costs and the overall level of taxation and prices.

The Insolvency and Bankruptcy Code (IBC) was a gamechanger by allowing assets to remain as viable units instead of being made piecemeal and by allowing creditors to initiate both liquidation and reorganisation and continuation of essential goods or services critical to protecting and preserving the value of the debtor during the proceedings. IBC also helps preserve and recover capital from failed assets, and ring-fences successful bidders of stressed assets from the risk of criminal proceedings. IBC has increased loan repayments and reduced delinquent accounts.

India is one of the few countries worldwide investing $1 trillion+ annually in the economy, government, and private sectors combined via gross capital formation. This amounts to a significant 31% of the nation’s GDP. Significant investments have been made to boost trade activities towards increasing the capacities of India’s ports, airports, freight, railways and other critical aspects of trade-related logistics. The trip from Bangalore to Delhi previously took four days, now it’s possible in two. Goods carriage speeds have exceeded 45kmph, from an average of 25kmph earlier. The Dedicated Eastern and Western Corridors for exclusive goods movement up and down the country have been game changers. Between GST and infrastructure development, supply chain costs are reducing from 14% of GDP to 8-9%.

Apart from improving the infrastructure itself, measures like electronic sealing of containers, electronic submission of supporting documents with digital signatures, machine-based automated clearance of imported goods and use of handheld devices for on-the-spot clearances have been taken to improve port operations and reduced turnaround times.

Several measures to simplify the process of starting businesses have been taken to boost entrepreneurship and business expansion. Forms like SPICe+ and AGILE PRO integrate various services like PAN, TAN, DIN and GSTN onto one, and are processed within 2-3 days. A single window for construction permits has also been introduced via OBPS.

The tax systems, both direct and indirect, have been automated, and efficiency has accelerated. More than 97% of tax assessments are completed within 30 days of filing. Digitalisation has significantly increased tax collections. Digitalisation across the economy has tremendously benefitted common citizens and their productivity – like accessing birth and death certificates, land records, and registering land purchases and other assets.

While there is tremendous progress in increasing the velocity of business and EoDB in India, addressing the following fundamental issues over the next five years will accelerate the ascent. Reforms are sorely needed in India’s justice system. Today commercial disputes take any time between 5-15 years to resolve, working its way through the courts. The system is overloaded with hardly 21 judges/million population, whereas the optimum number is between 50-100. Court proceedings often drag on with frequent adjournments. Lack of judicial capacity, archaic laws (despite repealing numerous old laws), and complicated processes are impeding justice and EoDB. While the Commercial Courts Act 2015 and its Amendment in 2018 provide for increasing the number of commercial courts across all levels – district, town and state, decreasing the monetary limit of commercial disputes to include a wider number of beneficiaries, and the use of IT and digitalisation services to hasten court operations, implementation must accelerate so commercial disputes can be settled within 2-3 years like in development.

Unnecessary tax disputes are hurting India’s brand equity. The quantum of tax disputes has increased from ₹4.5 lakh crore in 2014 to around ₹12 lakh crore in 2023. Many of these disputes are overturned on appeal, necessitating action to eliminate unnecessary high-pitch assessments. Accountability for wrong assessments and tax disputes must be increased, and broad administrative reforms must be enacted to curb arbitrary powers.

It is also incumbent on government organisations to respond to queries and give approvals within defined time limits to enhance EoDB. For example, while the RBI has complete autonomy on regulatory matters and conducts its role as the government’s banker admirably, its response time to queries or approvals required for business has been lacklustre. Many startups have relocated outside India due to the RBI’s lack of response in handling foreign currencies. RBI must create a KYC-driven depository system for investment in unlisted companies, as exists for listed companies.

Overall, the Indian government’s massive drive towards digitalisation, digital and financial inclusion, improvement of processes, and removal of unnecessary approvals over the past decade has paid rich dividends. India is steadily positioning itself as the world’s growth engine over the next 25-50 years. Accelerating India’s EoDB ranking is of vital importance to increase the velocity of business. Some measures taken over the next five years to improve judicial capacity, decrease tax disputes and ease the flow of foreign currency in and out of the country will have an outsized impact on the EoDB.

India is the Fourth-largest Equity Market Globally

India’s stock market has overtaken Hong Kong’s to rank as the fourth-largest

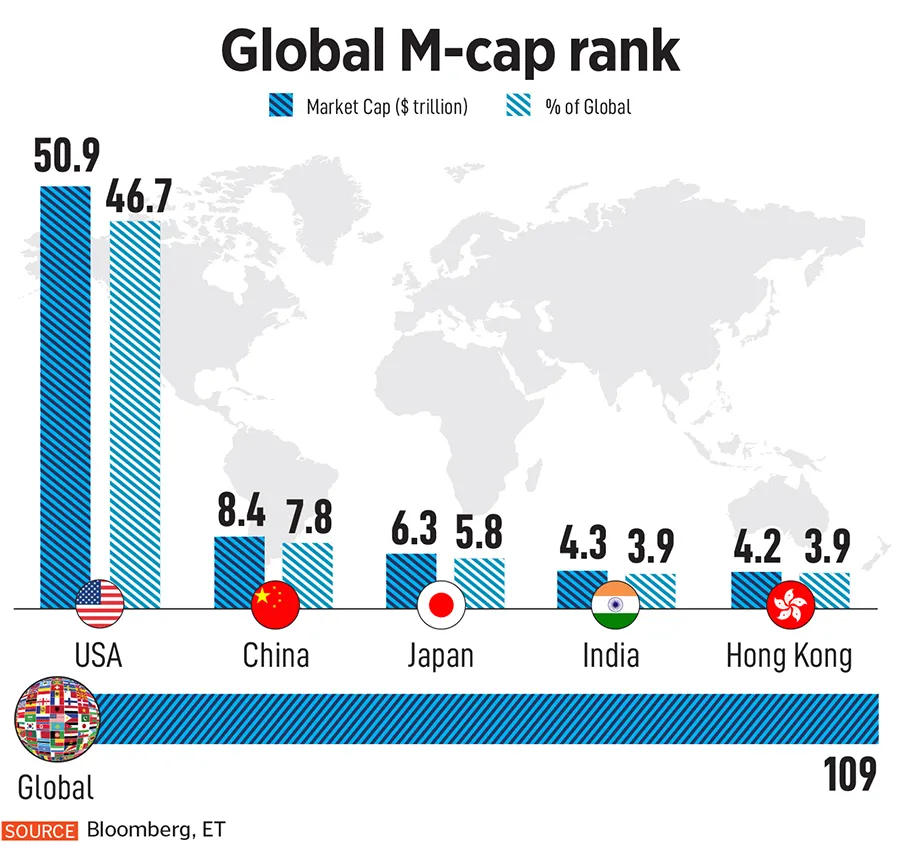

Fifty-four days after reaching a $4 trillion equity market capitalisation, India ascended to the fourth spot globally in January 2024, surpassing Hong Kong. India’s market cap rose to $4.33 trillion, edging out Hong Kong's $4.29 trillion. This advancement marks India's continued ascent in the global stock market rankings, having previously overtaken both France and the UK in June 2023, positioning it behind only the US, China, and Japan.

The US remains the largest stock market with a market cap of $50.86 trillion, followed by China at $8.43 trillion and Japan at $6.35 trillion. As of May 2024, India’s total market capitalisation stood at $4.7 trillion.

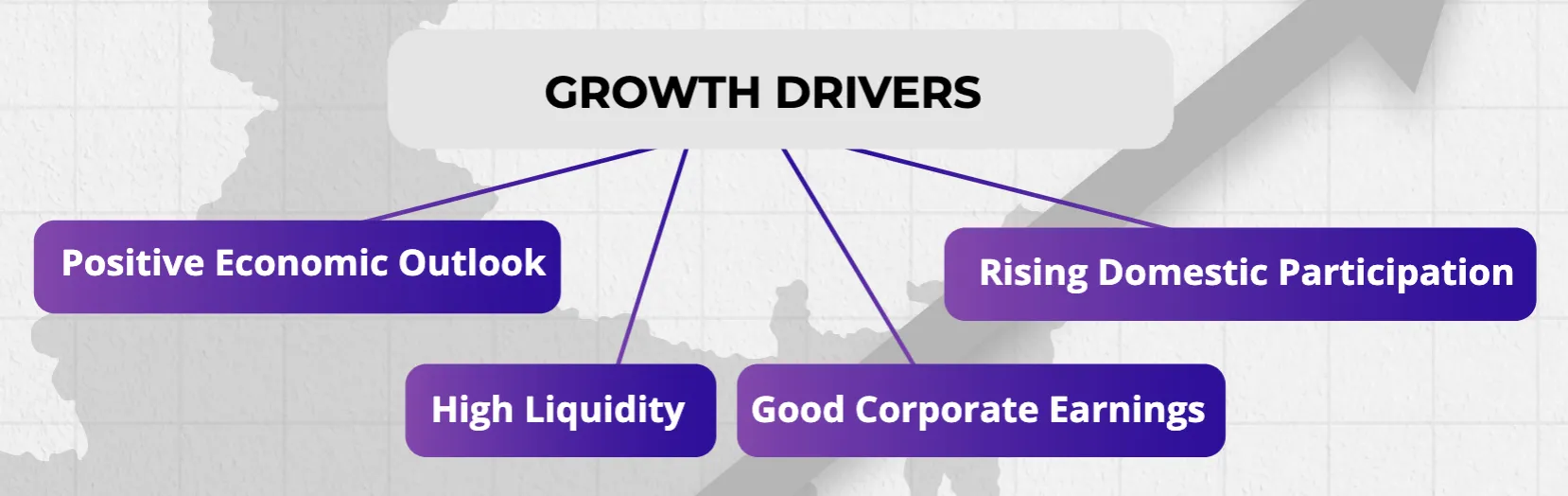

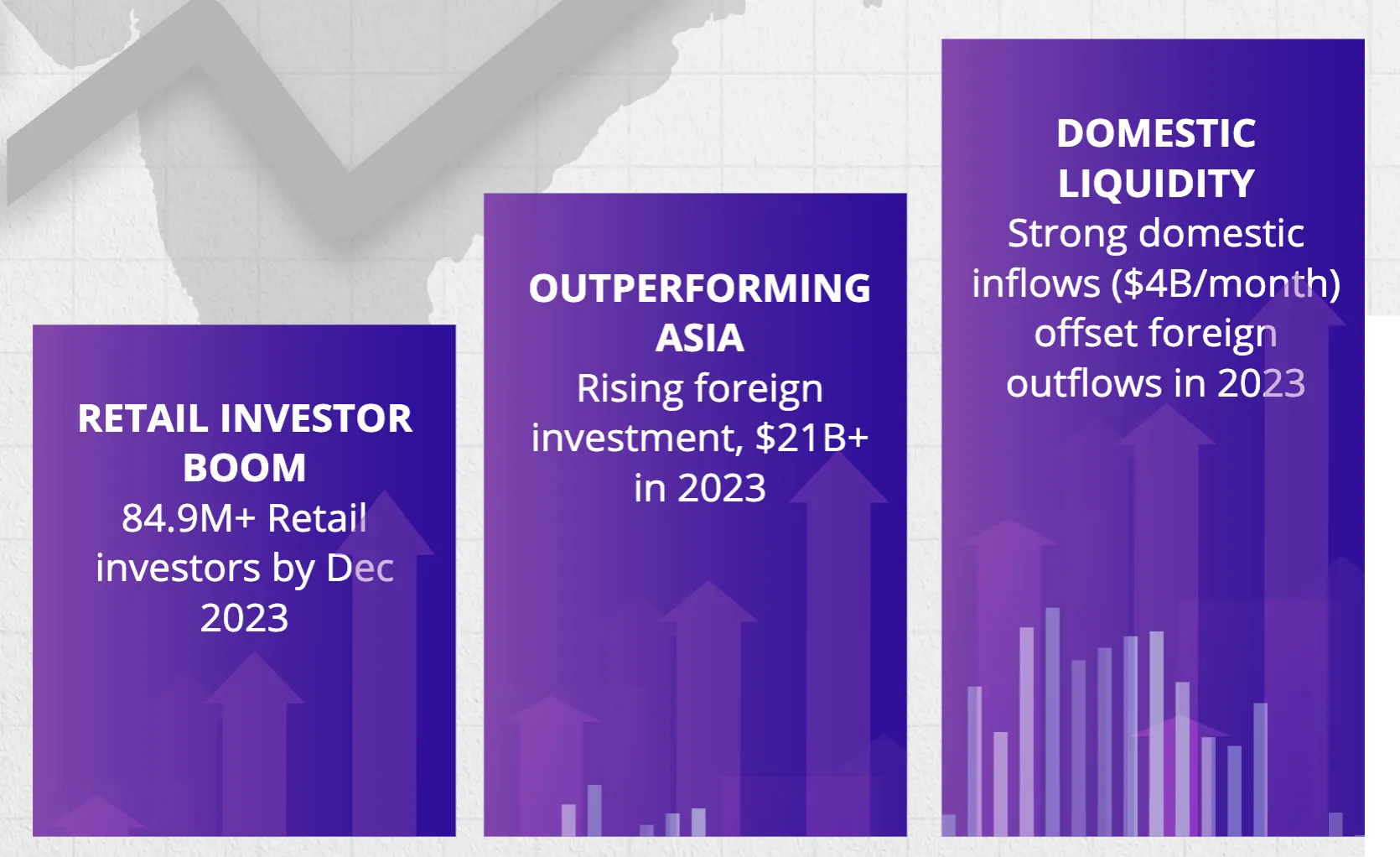

India's stock market is buoyed by optimism surrounding the country's economic prospects, enhanced liquidity, strong corporate earnings, and increasing domestic participation. As a standout performer in the Asia-Pacific region, India is witnessing significant growth in its retail investor base, supported by steady foreign institutional investor inflows and robust investor confidence. The number of registered stock market investors grew by 22.4% to 8.49 crore (84.9M) as of December 2023, up from 6.94 crore (69.4M) at the end of 2022, breaching the 8 crore mark (80M) within just eight months.

The Asian financial centre is seeing a decline in its status as a leading global location for initial public offerings (IPOs), with a significant slowdown in new listings in Hong Kong. In contrast, foreign investment in Indian stocks exceeded $21 billion in 2023, contributing to the S&P BSE Sensex Index in India securing gains for the eighth year in a row.

The inbound local liquidity of $4 billion monthly from SIPs, pension programs, and institutional allocations has provided a reliable substrate of support for the Indian markets. Even though net FII was outward in 2023, Indian markets have had some of their best quarters yet. Over CY 2023, the markets have accepted an IPO every 22 days, and the indices remain hungry for great Indian companies bringing new dimensions of the economy into the public markets.

The country’s large and consistent internal demand, more efficient market practices, rapid formalisation, intense capex expansion, growth in local manufacturing, and intentional shift towards renewable energy are multiplexing to support a national fabric of resilience against global uncertainty.

India Houses More Than 5% Of All Global +$1 Billion-Market Cap Companies

Moving beyond the unicorn milestone

The nation houses 525 stocks with a market capitalisation of over $1 billion as of January 2024. Of these, 137 were added just in the last year, up from 388 in January 2023. This is now 5.1% of global $1 billion stocks, having risen sharply from just over 2% in January 2015.

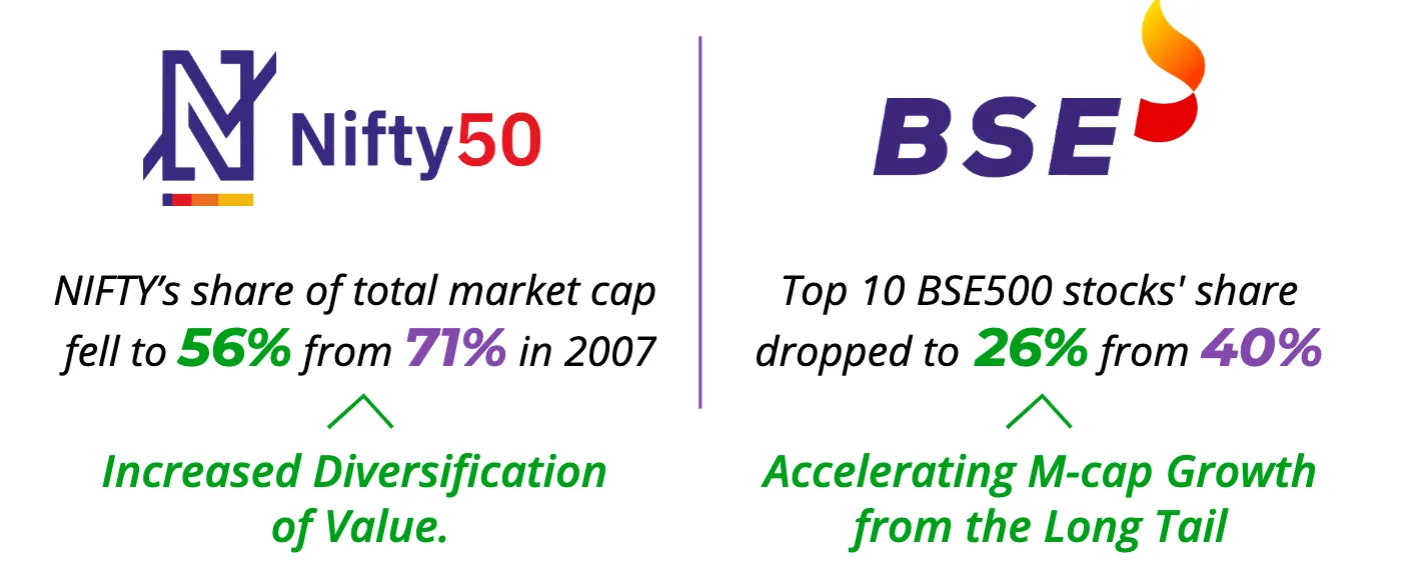

Barring the US, Indian stocks have outperformed all global and emerging markets over 10-year and 5-year periods. Over 2023, Indian stocks outperformed those in the US as well. A major contributor is broad-based growth, compared to a steep concentration in the US; the NIFTY’s share of total market capitalisation has fallen to 56% from 71% in 2007, the share of the Top 10 stocks in BSE500 is down to 26% from 40% in 2007, and the sectoral diversity of the 525 >$1 billion stocks is extensive, ranging from larger sectors like industrials, financials, materials, pharma, and IT services to an increasing long tail starting with utilities, staples, real estate, energy and telecom.

India’s stock market capitalisation exceeded that of Hong Kong and is now the fourth-largest equity market in the world. Broad-based economic growth, strong corporate earnings performance, a rapidly growing retail investor base, and sustained foreign capital inflows are some factors driving this growth. BSE-listed companies’ combined market cap now exceeds ₹400 lakh crore for the first time, doubling from ₹200 lakh crore just three years ago. As local capital flows continue to scale past $4 billion every month, India’s market capitalisation is expected to see sustained growth.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)

%20(1).jpg)

-p-500.webp)