Unlocking Value Through Innovation: A Strategic Guide to India's DSIR R&D Recognition Scheme for Startups

1: Decoding the DSIR RDI Recognition Framework

1.1. The Mandate and Strategic Objectives of DSIR Recognition

The Department of Scientific and Industrial Research (DSIR), operating under the Ministry of Science and Technology, was established in 1985 with a mandate to promote indigenous technology development, utilization, and transfer. Within this mandate, the Industrial R&D Promotion Programme (IRDPP) is a cornerstone initiative, and its "Recognition of in-house R&D Units (RDI)" scheme is the primary instrument for engaging with the private sector.

The core objective of the RDI Recognition scheme is to formalize and encourage genuine research and development activities within Indian industry. It is designed to bring a sharper focus to corporate R&D, strengthen the underlying infrastructure, and ensure that industrial innovation aligns with national technological and developmental goals. The scheme's significance is underscored by its unique position; it is described as the "only scheme in the entire government set-up for benchmarking the industrial R&D," making it the definitive national standard for what constitutes a legitimate corporate R&D centre. By providing a formal recognition framework, the government aims to create a virtuous cycle where companies are incentivized to invest in structured R&D, which in turn leads to innovation, increased competitiveness, and economic growth.

1.2. The Litmus Test: Defining "In-House R&D" vs. Routine Operations

A fundamental aspect of the DSIR scheme is its strict and clear definition of what constitutes Research and Development. This distinction serves as the primary gatekeeper for eligibility and is the most common point of failure for applicants. Misunderstanding this definition can lead to a rejected application, wasting significant time and resources.

According to DSIR guidelines, recognized in-house R&D units are expected to be engaged in innovative research and development activities directly related to the company's line of business. Eligible activities are characterized by their focus on novelty and improvement. These include:

- Development of new technologies, products, or processes.

- Substantial improvements in existing products, processes, or designs.

- Design and engineering of new solutions.

- Development of new methods for analysis, testing, and quality assessment.

- Research aimed at increasing efficiency in the use of resources, such as materials, energy, and capital equipment.

- Activities related to pollution control, effluent treatment, and waste recycling.

Conversely, the DSIR explicitly excludes activities that are routine, operational, or commercial in nature. These non-qualifying activities are critical to understand, as confusing them with genuine R&D is a frequent pitfall. Activities not considered R&D include:

- Market research and sales promotion.

- Operations and management research, work and methods studies.

- Routine testing and analysis for the purpose of operational process control or quality control (QC) and quality assurance (QA).

- Maintenance of day-to-day production and plant infrastructure.

The emphatic and repeated distinction between genuine R&D and routine QA/QC reveals the core philosophy of the DSIR's evaluation process. The department's primary filter is not the mere existence of a laboratory or technical staff, but the nature and intent of the work being performed. The focus is on activities that create new knowledge and capabilities, rather than those that simply verify existing standards.

A startup's assertion of having an "R&D team" must be rigorously vetted against these definitions. The fund's advisory role should therefore begin by helping founders articulate their technical work in the language of DSIR, emphasizing innovation, novelty, and substantive improvement, and clearly segregating these from routine verification and control processes.

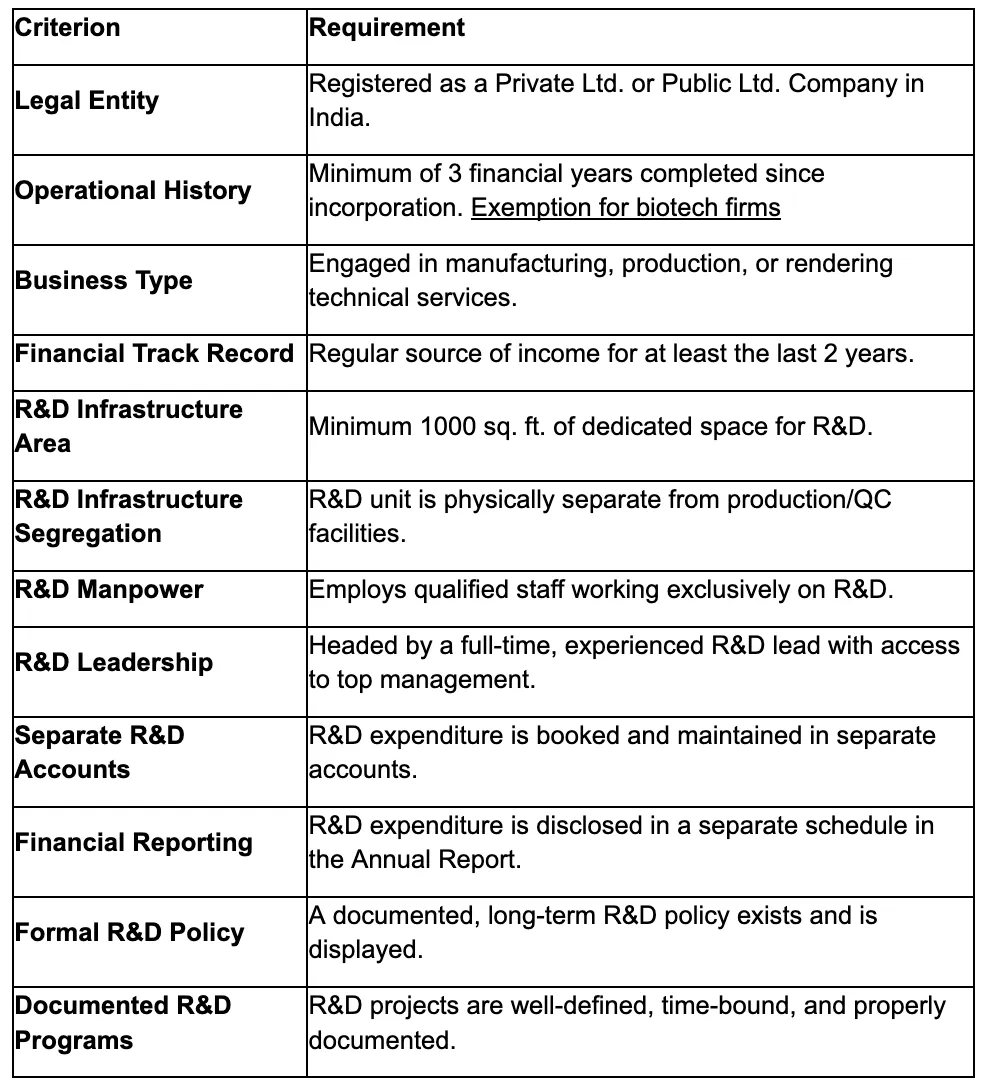

1.3. Comprehensive Eligibility Criteria for Corporate Entities

To qualify for DSIR recognition, companies must meet a stringent set of criteria related to their legal structure, operational history, business activities, and the specific setup of their R&D unit. These criteria ensure that the benefits are directed toward stable, committed, and genuinely innovative enterprises.

Company Structure: The applicant must be a Public Limited or Private Limited Company registered under the Companies Act, 2013 (or the preceding Act of 1956). This explicitly excludes other business structures such as Limited Liability Partnerships (LLPs) and proprietorships.

Operational History: A company is generally eligible for consideration only after the completion of three financial years from its date of incorporation. This requirement ensures that the applicant has a proven track record of operations and is not a nascent entity without established business activities.

Business Activity: The company must be actively engaged in manufacturing, production, or the provision of technical services. Companies that are purely service-oriented in non-technical domains are typically not considered eligible.

Financial Stability: Applicants are required to demonstrate a regular source of income for at least the last two years, substantiating their capacity to sustain business operations and fund ongoing R&D efforts.

R&D Infrastructure: A dedicated and identifiable infrastructure for R&D is mandatory. This includes a minimum physical area of at least 1000 square feet for R&D activities. Furthermore, this R&D unit must be physically segregated from routine production and quality control areas. This can be achieved by locating it in a separate room, on a separate floor, or in a completely separate building.

R&D Manpower: The R&D unit must be staffed by qualified personnel engaged exclusively in research and development. It must be headed by a full-time, qualified, and experienced R&D leader who has direct access to the company's Chief Executive or Board of Directors, ensuring that R&D is a strategic priority at the highest level of the organization.

R&D Accounting and Policy: The company must maintain separate books of accounts for all R&D expenditures, both capital and revenue. These expenditures should be clearly reflected in separate schedules within the company's Annual Report and Statement of Accounts. Additionally, the company is expected to have a formally articulated long-term R&D policy, which should be prominently displayed within the R&D unit.

To facilitate a quick assessment for startups and investors, the following checklist consolidates these requirements.

1.4. Special Provisions: The Biotech Startup Exemption

Recognizing the long gestation periods and high-risk nature of the biotechnology sector, the DSIR has carved out a significant exception to its standard eligibility criteria. For biotech startups, the requirement of a minimum three-year operational history is waived. This special provision is designed to promote entrepreneurship and accelerate innovation in a field deemed critical to national strategic interests.

To qualify for this exemption, a biotech startup must meet a different set of criteria focused on potential and structure, rather than history:

- The company must be engaged in high-end research with a clear scope for generating valuable Intellectual Property (IP) and future revenue.

- It must have qualified R&D manpower and at least a basic minimum R&D infrastructure in place.

- The startup should have focused research objectives based on innovative technologies, a clear business model, and identified sources of funding for sustainability.

- Crucially, the company must furnish evidence of collaboration, such as agreements or MOUs, with an incubator, technology park, or a similar institution.

1.5. Global Innovation, Local Recognition: Eligibility for Foreign-Owned Indian Subsidiaries

The DSIR RDI Recognition scheme is not limited to domestically owned companies. In a clear move to encourage R&D investment from global corporations, the scheme is open to foreign companies operating in India, provided they are registered as a company in India under the Companies Act. This means that an Indian subsidiary of a foreign parent company is fully eligible to apply for and receive recognition for its in-house R&D unit.

However, a key jurisdictional requirement is that the R&D facility itself must be physically located within India. An Indian company cannot seek recognition for an R&D centre that is based outside the country.

2: The Value Proposition: Analysing the Financial and Strategic Impact

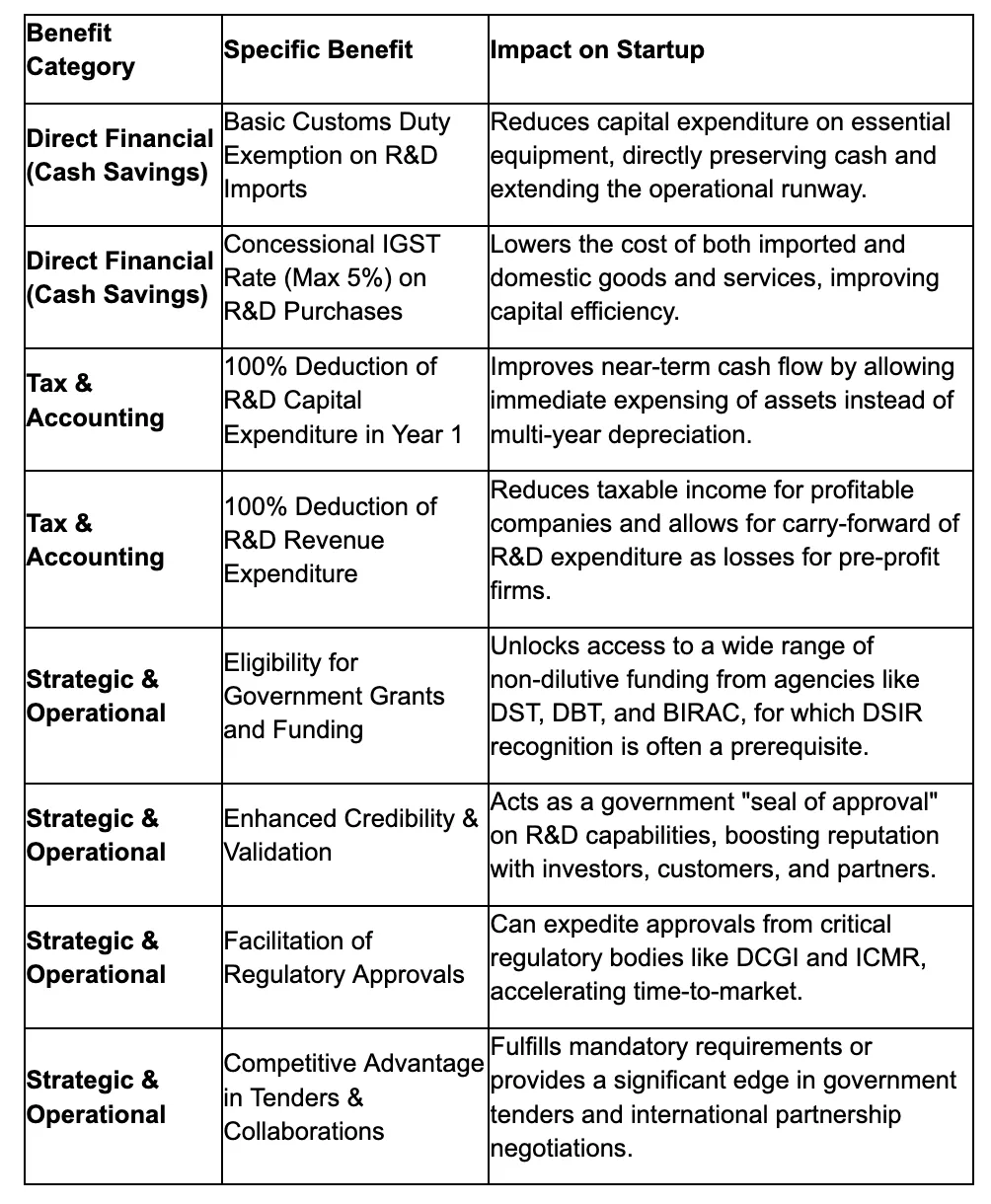

The DSIR RDI Recognition benefits can be categorized into direct fiscal incentives that preserve cash, tax and accounting advantages that improve financial reporting, and strategic multipliers that unlock new opportunities.

2.1. Direct Fiscal Incentives: A Granular Analysis

The direct fiscal incentives offered by DSIR recognition translate into an extended runway and reduced cash burn.

Customs Duty Exemption: Recognized R&D units are eligible for an exemption from Basic Customs Duty on the import of specified equipment, instruments, spares, and consumables required for R&D purposes. This is a significant benefit for deep-tech, hardware, or life sciences startups that often rely on specialized, high-cost equipment available only from international markets. For companies in the pharmaceutical and biotechnology sectors, this benefit is even broader, covering duty-free import of specified goods for both R&D and production activities.

GST Concession: In addition to customs duty exemption, the scheme provides a concessional rate for the Integrated Goods and Services Tax (IGST). For purchases made for the recognized R&D unit, the maximum applicable IGST is capped at 5%. This reduces the cost of both imported and domestically procured goods and services for R&D.

Accelerated Depreciation: Perhaps one of the most impactful benefits for a startup's cash flow is the ability to claim a 100% deduction on capital expenditure for R&D in the very first year. Standard accounting practices require companies to depreciate capital assets over several years. This provision allows the entire cost of R&D equipment to be expensed in the year of purchase, significantly reducing taxable income for profitable companies and improving near-term cash flow dynamics for all.

2.2. The Evolution of Tax Deductions: Understanding Section 35(2AB) and the Current 100% Deduction Regime

To fully appreciate the current tax benefits, it is essential to understand their historical context. For many years, the centrepiece of the DSIR scheme's fiscal incentives was the "weighted tax deduction" under Section 35(2AB) of the Income Tax Act, 1961. This provision allowed eligible companies to deduct more than their actual R&D expenditure from their taxable income. Initially, this "super-deduction" was as high as 200%, later rationalized to 150%. This was an extremely attractive incentive for large, profitable corporations, as it substantially lowered their tax liability.

However, as part of a broader fiscal policy to phase out exemptions and lower corporate tax rates, the weighted deduction was discontinued. Effective from the assessment year beginning on or after April 1, 2021, the deduction under Section 35(2AB) has been reduced to 100% of the expenditure incurred.

2.3. Beyond Tax: The Strategic Multiplier Effect

The most profound benefits of DSIR recognition are often strategic and non-fiscal. The certificate acts as a key that unlocks a range of opportunities, enhancing a company's credibility, market access, and ability to secure further funding.

Gateway to Further Funding: This is arguably the most powerful non-fiscal benefit. DSIR recognition is frequently a mandatory or highly preferred eligibility criterion for companies seeking R&D grants and other forms of financial support from a host of other government departments and agencies. These include the Department of Science and Technology (DST), the Department of Biotechnology (DBT), the Biotechnology Industry Research Assistance Council (BIRAC), the Council of Scientific and Industrial Research (CSIR), and the Technology Development Board (TDB). In essence, the DSIR certificate serves as a passport to the broader ecosystem of non-dilutive government funding.

Enhanced Credibility and Market Access: The recognition certificate is a powerful third-party validation of a company's technical and R&D capabilities. This government-backed endorsement significantly boosts credibility in various contexts:

Regulatory Approvals: It can facilitate and expedite regulatory approvals from bodies such as the ICMR, DCGI, and the National Seed Board, which is particularly crucial for startups in the health-tech, med-tech, and agri-tech sectors.

Government Tenders: In public procurement, having a DSIR-recognized R&D unit can be a mandatory requirement or a significant advantage, proving the company's technical competence.

Partnerships and Collaborations: The certificate enhances a company's standing in negotiations with potential international partners, collaborators, and even customers, who see it as a mark of quality and innovation.

The following table provides a consolidated summary of the full spectrum of benefits.

2.4. A Framework for Financial Modelling: Quantifying the Impact

To translate these benefits into tangible financial metrics, VCs and startups can build a simple model to quantify the impact of DSIR recognition. This model should focus primarily on the direct cash savings, which have the most immediate effect on a startup's financial health.

Consider a hypothetical deep-tech startup that needs to establish its R&D lab. The planned capital expenditure on imported equipment is ₹5 crores.

Scenario A: Without DSIR Recognition

Cost of Equipment: ₹5,00,00,000

Assumed Basic Customs Duty + Cess (~18%): ₹90,00,000

Assumed IGST (18% on): ₹1,06,20,000

Total Cash Outflow: ₹6,96,20,000 (Note: IGST is typically available as an input tax credit, but the initial cash outflow is high).

Scenario B: With DSIR Recognition

Cost of Equipment: ₹5,00,00,000

Basic Customs Duty: ₹0

Concessional IGST (5% on Cost): ₹25,00,000

Total Cash Outflow: ₹5,25,00,000

In this illustrative scenario, DSIR recognition results in a direct reduction in initial cash outflow of ₹1.71 crores. For a startup, this can translate to several additional months of operational runway, the ability to hire more engineers, or the capacity to conduct more experiments.

Beyond this direct impact, the financial model can also incorporate the potential value of non-dilutive grants unlocked by the recognition. If the certificate enables the startup to secure a ₹2 crore grant from BIRAC, the net positive impact on the company's finances is even more profound. While the 100% accelerated depreciation benefit is more complex to model for a pre-profit company, it contributes to the creation of deferred tax assets on the balance sheet, which holds future value.

3: A Founder's Playbook: Navigating the DSIR Application Lifecycle

Securing DSIR recognition requires a methodical and well-documented approach. This section provides a step-by-step playbook for founders and their teams to navigate the entire process, from initial preparation to post-recognition compliance.

3.1. The End-to-End Application Process: A Step-by-Step Walkthrough

The application process, while detailed, is straightforward and can be broken down into five key stages.

Step 1: Preparation & Segregation: This is the most critical foundational step. Before even beginning the application, the company must ensure its R&D activities are clearly identified and segregated from routine operations. This segregation must be both physical (a dedicated space for R&D) and financial (separate ledgers or cost centres for all R&D-related expenses). Meticulous record-keeping of R&D projects, objectives, and outcomes should be standard practice.

Step 2: Application Submission: The current submission process has been streamlined. While older guidelines refer to an online portal followed by a hard copy submission , the most recent directives indicate a move to an email-based system. The applicant must compile the complete application, including all annexures, into a single PDF file signed by the Managing Director or a whole-time Director. This file, not exceeding 20 MB in size, is then emailed to the designated DSIR email address: rdi-fresh@gov.in for new applications and rdi-renewal@gov.in for renewals. No hard copy is required.

Step 3: Screening & Verification: Upon receipt, DSIR officials conduct an initial screening of the application. They check for completeness, adherence to the eligibility criteria, and clarity in the description of R&D activities. If the application is incomplete or unclear, it may be rejected at this stage.

Step 4: The DSIR Interview and/or On-Site Visit: If the application passes the initial screening, DSIR may schedule an interaction. This can be a formal discussion at the DSIR offices in New Delhi or, in some cases, an on-site visit to the company's R&D facility by a team of DSIR representatives and domain experts. During this stage, the company's leadership will be expected to present their R&D activities, future plans, and provide a video walkthrough of the laboratory.

Step 5: Issuance of Certificate: Based on the application, the discussion, and any visit reports, DSIR makes a final decision. If successful, a recognition certificate is issued. The recognition is typically valid for a period of three years, terminating on the 31st of March of the third financial year. The entire process, from submission to certification, generally takes around two to three months, provided all documentation is in order.

3.2. Assembling the Application Dossier: A Best-Practice Checklist

A comprehensive and well-organized application dossier is crucial for a smooth evaluation process. The following checklist, compiled from official guidelines, outlines the essential documents required :

Covering Letter: A formal letter on the company's letterhead, signed by the MD/Director, clearly stating the purpose of the application (fresh recognition or renewal).

Signed Application Form: The complete, duly filled application proforma, signed by the MD or a whole-time Director.

Note on R&D Activities: A detailed note that is the heart of the application. It should cover:

- Past R&D achievements and completed projects.

- Detailed descriptions of ongoing R&D projects, including objectives, methodologies, and timelines.

- A clear roadmap of future R&D programs and the company's long-term vision.

Details of R&D Personnel: A list of all scientific and technical personnel engaged exclusively in R&D, including their names, qualifications, designations, and experience.

Details of R&D Infrastructure: A comprehensive list of all major R&D equipment and facilities, specifying the date of installation and the original value of each item.

Layout Drawing: A clear architectural or schematic drawing showing the layout of the R&D unit and its location relative to the main plant or production area, demonstrating its physical segregation.

Latest Audited Annual Report: The complete annual report for the latest financial year. It is critical that this report contains a separate schedule clearly detailing the capital and revenue expenditure on R&D.

Supporting Presentations: A corporate presentation and a separate, detailed presentation on the R&D unit and its activities.

Walk-in Video: A short, clear video tour of the R&D facility, showcasing the infrastructure, equipment in operation, and the team at work. A link to this video should be provided.

Company Documents: A copy of the Memorandum & Articles of Association and the company's PAN card. For renewals, a copy of the previous recognition letter is also required.

3.3. Mastering the DSIR Interview and On-Site Verification

The interaction with the DSIR committee is a critical evaluation stage. Success depends on clear communication and credible demonstration of the company's commitment to R&D.

Leadership Presence is Non-Negotiable: DSIR explicitly discourages the presence of external consultants in formal meetings. The company must be represented by its own senior leadership, typically the Managing Director/CEO and the Head of R&D. This demonstrates that R&D is a core strategic function driven from the top.

Articulate the R&D Vision: Be prepared to clearly and concisely present the company's long-term R&D policy and vision. The committee wants to see that R&D is not an ad-hoc activity but a structured, strategic imperative for the business.

Demonstrate Process and Documentation: Showcase the well-defined, time-bound nature of your R&D programs. Have documentation, project plans, and records of experiments readily available to demonstrate a systematic approach to research.

Showcase Financial Segregation: Be ready to explain how R&D accounts are maintained separately and how expenditure is tracked and reported. This reinforces the integrity of the R&D function and its financial independence from routine operations.

3.4. De-risking the Application: Common Pitfalls and Mitigation Strategies

Many applications are rejected due to avoidable mistakes. Awareness of these common pitfalls can significantly de-risk the application process.

Pitfall 1: Confusing R&D with QA/QC. This is the most frequent error.

Mitigation: Before writing the application, rigorously apply the definitions from Section 1.2. Create two distinct lists of activities: "Core R&D" and "Operational/QC." The application narrative should focus exclusively on the former, using language that emphasizes innovation, experimentation, and the creation of new knowledge.

Pitfall 2: Inadequate or Vague Documentation. An application with generic project descriptions and incomplete data will be quickly dismissed.

Mitigation: Be specific and data-driven. For each R&D project, describe the problem statement, the hypothesis, the methodology, the results (even if partial), and the next steps. Quantify achievements where possible (e.g., "improved process efficiency by 15%," "developed a new algorithm that reduced processing time by 30%"). Meticulously follow the document checklist in Section 3.2.

Pitfall 3: Insufficient Segregation of R&D. A lack of clear physical and financial separation between R&D and production raises red flags.

Mitigation: Ensure the R&D lab is in a physically distinct, access-controlled area. The layout drawing submitted should clearly illustrate this separation. Similarly, work with the finance team to create dedicated cost centres and general ledger codes for all R&D expenses. The separate schedule in the annual report is non-negotiable proof of this financial segregation.

3.5. The Journey After Recognition: Compliance, Reporting, and Renewal

Receiving the DSIR certificate is the beginning, not the end, of the process. Maintaining the recognition and maximizing its benefits requires ongoing compliance.

Validity and Renewal: The recognition certificate is typically valid for three years. To ensure continuity of benefits, the application for renewal must be submitted at least three months prior to the expiry date of the current recognition.

Continuous Reporting: The company must continue to maintain separate R&D accounts and reflect this expenditure clearly in a separate schedule in its annual reports for every subsequent year.

Reporting for Fiscal Benefits: To claim the 100% tax deduction on R&D expenditure under Section 35(2AB), there is an additional layer of compliance. The company must electronically file Form 3CK to seek approval for its R&D facility from DSIR. Subsequently, for each financial year, it must file Form 3CL, which is a report of expenditure on scientific research, to be submitted to DSIR for verification and approval. This two-step process (recognition followed by approval and annual reporting) is essential for availing the income tax benefits.

4: The Evolving Landscape: Synergies and Future Outlook

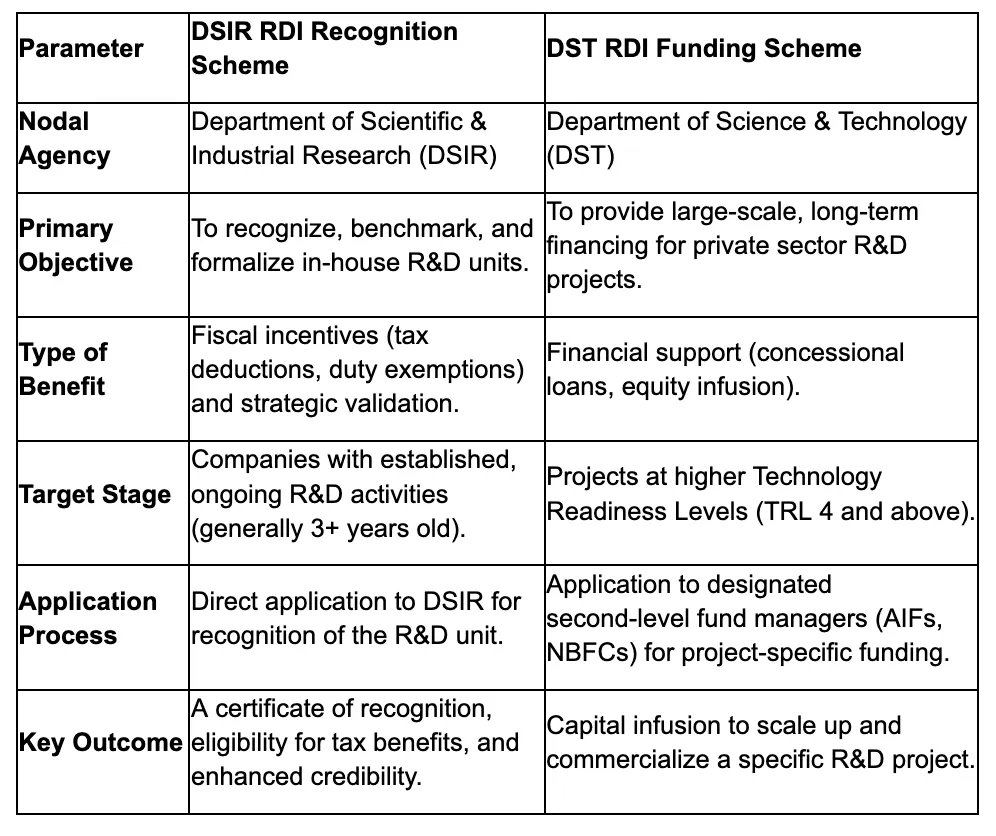

India's R&D incentive landscape is undergoing a significant transformation. The established DSIR Recognition scheme now coexists with a new, large-scale funding initiative. Understanding the interplay between these schemes is critical for any technology startup seeking to leverage government support for its innovation journey.

4.1. The New Frontier: The DST Research, Development, and Innovation (RDI) Funding Scheme

In a landmark move in July 2025, the Union Cabinet approved the Research, Development, and Innovation (RDI) Scheme, a transformative initiative managed by the Department of Science & Technology (DST). It is crucial to note that while it shares the "RDI" acronym, this is a separate and distinct program from the DSIR's recognition scheme.

Objective: The primary goal of the DST RDI scheme is to catalyze private sector investment in R&D by overcoming the funding challenges that often hinder innovation, a problem often referred to as the "valley of death". It specifically targets projects that are at a more advanced stage, typically at Technology Readiness Levels (TRLs) 4 and above, moving them closer to commercialization.

Corpus and Mechanism: The scheme is backed by a massive ₹1 lakh crore corpus. Its funding mechanism is structured in two tiers. At the first level, a Special Purpose Fund (SPF) housed within the Anusandhan National Research Foundation (ANRF) will receive a 50-year interest-free loan from the government. This SPF will then allocate capital to second-level fund managers, such as Alternate Investment Funds (AIFs), Non-Banking Financial Companies (NBFCs), and other focused research organizations. These fund managers will, in turn, provide funding to eligible R&D projects in the private sector.

Modes of Financing: The primary mode of financing will be long-term loans at low or nil interest rates. For startups, the scheme also allows for funding in the form of equity infusion, and it will support the creation of a Deep-Tech Fund of Funds.

Focus Areas: The scheme is designed to bolster India's capabilities in strategic and sunrise sectors vital for national development and global competitiveness. These include Artificial Intelligence, quantum computing, robotics, space, biotechnology, clean energy, and digital agriculture.

To eliminate any confusion, the following table provides a clear comparative analysis of the two schemes.

4.2. The Critical Nexus: Analyzing DSIR Recognition as a Gateway to the ₹1 Lakh Crore DST Fund

While the official guidelines for the new DST RDI Funding Scheme are still evolving, a logical and strategic connection to the existing DSIR recognition scheme is highly probable. The DSIR recognition certificate is poised to become the "golden ticket" for startups seeking to access this new, massive pool of capital.

This conclusion is based on a clear chain of reasoning. First, the established guidelines for the DSIR scheme have historically and explicitly stated that its recognition is a prerequisite for receiving funds from other government agencies, including the DST. This precedent establishes a clear inter-agency linkage.

Second, the implementation structure of the new DST scheme relies on second-level fund managers like AIFs and NBFCs to perform the crucial task of technical and commercial due diligence on R&D projects. These fund managers will need a credible, standardized, and efficient mechanism to vet the R&D capabilities of applicant companies.

Third, the DSIR recognition process is the government's own rigorous, time-tested benchmark for validating a company's R&D infrastructure, processes, and personnel. It serves as a pre-vetted stamp of approval.

Therefore, it is the most logical and efficient pathway for these fund managers to use DSIR recognition as a primary filter or, at a minimum, as a significant positive signal when evaluating funding applications. A startup approaching a fund manager with a DSIR certificate in hand is presenting a pre-vetted, lower-risk proposition. Its R&D credentials have already been validated by another arm of the government. This will almost certainly give it a substantial advantage over a non-recognized applicant. Consequently, securing DSIR recognition today is not just about immediate tax benefits; it is a critical strategic move to prepare for and gain preferential access to the far larger funding opportunities of tomorrow.

4.3. Building a Moat: Integrating DSIR Benefits with Other Incentives

The value of DSIR recognition is further amplified when its benefits are "stacked" with other government incentives, creating a comprehensive support structure around a startup's innovation activities.

Startup India Initiative: A company can simultaneously be an "eligible start-up" under the Startup India program and have a DSIR-recognized R&D unit. This would allow it to avail the three-year 100% tax holiday on profits under Startup India, while also benefiting from the customs duty exemptions and accelerated depreciation on its R&D expenditure through the DSIR scheme.

Patent Box Regime: This creates a powerful full-cycle incentive. A company can use the benefits of its DSIR-recognized R&D unit to lower the cost of developing a new technology. Once that technology is developed and patented in India, the company can then avail the concessional 10% tax rate on any royalty income generated from that patent under the Patent Box regime. This synergy supports the entire innovation lifecycle, from the initial R&D investment (supported by DSIR) to the commercialization of the resulting intellectual property (supported by the Patent Box).

By strategically combining these schemes, a startup can build a significant competitive moat, leveraging government support to reduce costs, accelerate innovation, and enhance profitability.

5: Strategic Recommendations and Implementation Roadmap

Based on the comprehensive analysis of the DSIR RDI Recognition scheme and its position within India's evolving innovation policy landscape, the following actionable recommendations are provided for both the venture capital fund and its portfolio companies.

5.1. Startups: A Phased Roadmap for Achieving and Maximizing DSIR Recognition

For a startup, the journey to DSIR recognition should be a planned, multi-phase process that begins long before the application is submitted.

Phase 1: Early-Stage Structuring (Pre-Eligibility): Even before meeting the three-year operational requirement, a startup should begin laying the groundwork for a future DSIR application. This proactive approach involves:

- Financial Discipline: From day one, implement separate accounting codes or cost centres for all R&D-related expenses, including salaries, materials, and equipment.

- Physical Demarcation: As soon as a dedicated lab or workspace is established, ensure it is physically separate from other operations and clearly designated as the R&D centre.

- Meticulous Documentation: Institute a rigorous process for documenting all R&D projects. Maintain detailed records of objectives, experiments, data, results, and project timelines.

Phase 2: Application Readiness (3-6 Months Prior to Eligibility): As the company approaches the three-year mark, it should begin actively compiling the application dossier. This involves gathering all the documents outlined in Section 3.2, finalizing the R&D narrative, preparing the corporate and R&D presentations, and shooting the R&D facility video tour.

Phase 3: Application & Follow-up (At Eligibility): Once eligible, submit the complete application via the designated email channel. The leadership team should then prepare thoroughly for the potential interview or on-site visit, ensuring they can confidently articulate the company's R&D strategy and achievements.

Phase 4: Maximization & Leverage (Post-Recognition): Securing the certificate is the trigger for maximizing its value. The company should immediately:

- Apply for the necessary customs duty exemption certificates (CDECs) for planned R&D imports.

- Actively scan for and apply to government grants and funding schemes where DSIR recognition is a prerequisite.

- Incorporate the DSIR recognition status into all external communications, including marketing materials, investor relations updates, partnership proposals, and tender documents, to leverage its credibility-enhancing power

Conclusion

Securing DSIR recognition is a strategic investment for any innovation-led startup in India. It requires a dedicated effort, but the long-term benefits in terms of financial savings, enhanced credibility, and access to funding are well worth it.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)

-p-500.webp)

.jpg)